Key Events This Week: Core PCE, GDP, And Lots Of Earnings

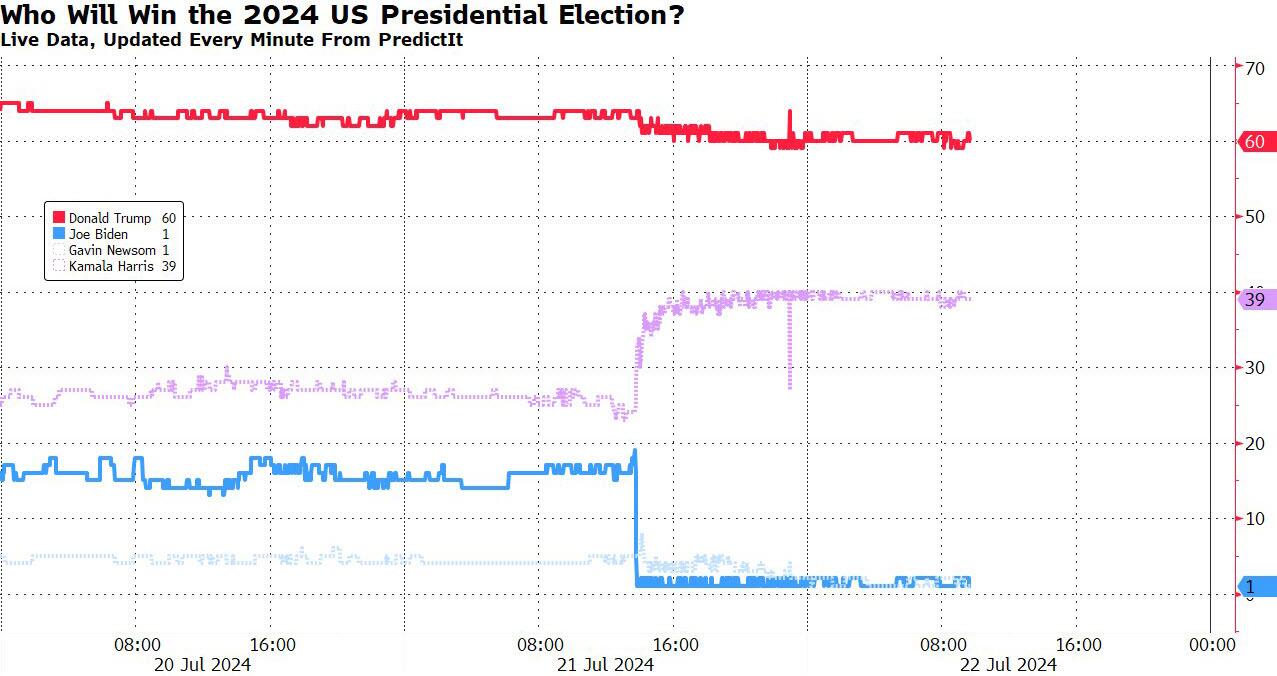

As we head into another week full of unknowns, DB’s Jim Reid notes this morning that one question that we don’t need to ask anymore is whether you think Joe Biden will be the Democratic Party nominee for President in November. On Friday speculation was rife that he would stand down as early as the weekend but bullish remarks by Biden on Saturday morning put some doubts to that speculation. However by Sunday afternoon Biden had unexpectedly withdrawn – through a tweet, and has yet to make any public appearance – and endorsed Kamala Harris. While it seems difficult to see a path for someone to pip her to the nomination, we are in uncharted territory so you couldn’t completely rule it out. The Democratic convention starts on August 19th so if someone was going to challenge they’d need to be building up momentum well ahead of that. Unless there was a groundswell of support for that candidate it seems a very high hurdle to supplant Harris. The Clintons have endorsed Harris even if Obama hasn’t – he is reportedly saving his nomination for his ‘wife’ – although his practise is not to do so until a nomination has been secured. Overnight, potential rivals Newsom and Buttigieg have also thrown their support behind Harris, although don’t be surprised if they reverse in the last minute. In terms of the polls, the match-up between Trump and Harris has been slightly narrower than with Biden in recent times with Trump 1.9pp ahead at the national level instead of 3pp according to Real Clear Politics poll aggregates. However with the attention now likely to be firmly on Harris this could move notably in either direction over the next few days and weeks. Perhaps for now it slightly reduces the impetus for Trump trades but there’s a long way to go.

{kind=link}

Political thriller aside, and as we await to see if Biden will really hold a press conference – and is, in fact, alive and not held hostage by Democratic sponsors – the other main events this week all point to Friday’s US core PCE deflator. En route to this,

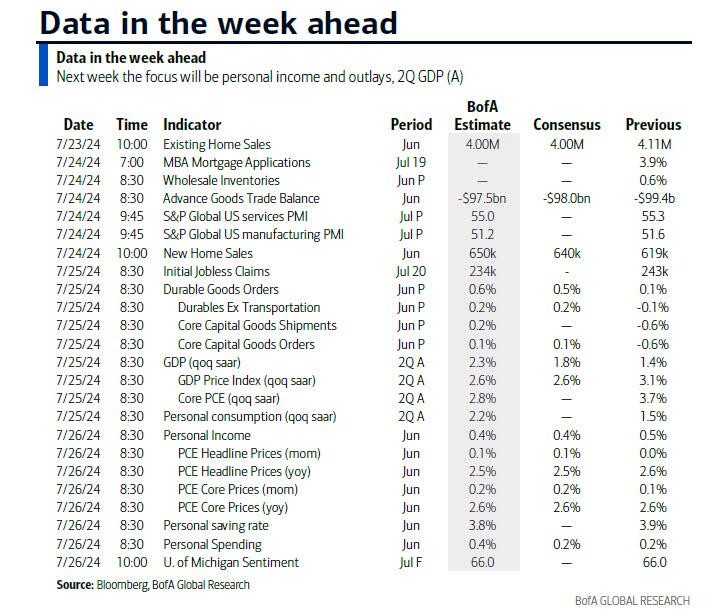

the main other highlights are US Q2 GDP on Thursday, the global flash PMIs and the Bank of Canada rate decision on Wednesday.

{kind=link}

With the core PCE deflator, DB economists expect a 0.14% MoM reading given the CPI and PPI components that feed into it. There could be some downward revisions to prior months that could edge this month up nearer to 0.2% so one to watch as a whole rather than the June number alone. The base case at DB is that the YoY rate will dip to 2.5% which is below the Fed’s YE ’24 prediction of 2.8% at their June FOMC. However the economists point out that base effects from low H2 prints last year will make further progress much more challenging. Nevertheless the recent run, especially in rents, suggest that the Fed will be having increasing confidence that inflation is moving back closer to 2%. For Q2 US GDP, economists expect a 1.9% growth print, although with durable goods out at the same time there might be a bit more uncertainty than usual.

We also have a big week for earnings that includes Tesla and Alphabet which will become the first of the “Magnificent Seven” to report in the latest round of results; tomorrow we also get the latest earnings out of LVMH. Strategists at Morgan Stanley said companies in Europe have made a positive start to the second-quarter reporting season, with 29% beating profit expectations, but the tone was less positive on Monday, with Ryanair plunging after the Irish budget carrier cut its outlook for ticket prices in the crucial summer travel period.

{kind=link}

Don’t expect to hear from Fed officials as they are on their blackout period ahead of next week’s FOMC.

Below, courtesy of DB, is a day-by-day calendar of events

Monday July 22

Data: US June Chicago Fed national activity index, France June retail sales, China 1-yr and 5-yr loan prime rates Earnings: SAP, Verizon Communications, Cadence Design Systems, NXP Semiconductors, IQVIA, Nucor, Ryanair

Tuesday July 23

Data: US July Philadelphia Fed non-manufacturing activity, Richmond Fed manufacturing index, business conditions, June existing home sales, Eurozone July consumer confidence

Central banks: ECB’s Lane speaks

Earnings: Alphabet, Tesla, Visa, LVMH, Coca-Cola, Danaher, Texas Instruments, General Electric, Comcast, Lockheed Martin, HCA Healthcare, Freeport-McMoRan, Spotify, General Motors

Auctions: US 2-yr Notes ($69bn)

Wednesday July 24

Data: US, UK, Japan, Germany, France and Eurozone July PMIs, US June wholesale inventories, advance goods trade balance, new home sales, Germany August GfK consumer confidence

Central banks: BoC decision, Fed’s Bowman and Logan speak, ECB’s Guindos and Lane speak

Earnings: Thermo Fisher Scientific, IBM, ServiceNow, NextEra Energy, AT&T, SK Hynix, Boston Scientific, Fiserv, Iberdrola, Equinor, Chipotle Mexican Grill, Porsche, Ford, Newmont, Kering, Renault, Carrefour

Auctions: US 2-yr FRN ($30bn), 5-yr Notes ($70bn)

Thursday July 25

Data: US Q2 GDP, June durable goods orders, July Kansas City Fed manufacturing activity, initial jobless claims, Japan June PPI services, Germany July Ifo survey, France July manufacturing confidence, Q2 total jobseekers, Eurozone June M3 Central banks: ECB’s Nagel speaks

Earnings: AbbVie, Nestle, Roche, AstraZeneca, Hermes, TotalEnergies, Unilever, Honeywell, RTX, Sanofi, EssilorLuxottica, Enel, Vinci, Stellantis, Dassault Systemes, Valero Energy, Keurig Dr Pepper, Dow, STMicroelectronics, Anglo American

Auctions: US 7-yr Notes ($44bn)

Friday July 26

Data: US June PCE, personal income, personal spending, July Kansas City Fed services activity, Japan July Tokyo CPI, France July consumer confidence, Italy July consumer confidence index, manufacturing confidence, economic sentiment

Central banks: ECB June consumer expectations survey

Earnings: Keyence, Air Liquide, Bristol-Myers Squibb, Colgate-Palmolive, Mercedes-Benz, Holcim, Eni, BASF, Capgemini, BT

* * *

Finally, looking at just the US, Goldman notes that the key economic data releases this week are the durable goods report and the Q2 GDP advance release on Thursday, and core PCE inflation on Friday. Fed officials are not expected to comment on monetary policy this week, reflecting the blackout period in advance of the FOMC meeting on July 30-31.

Monday, July 22

No major data releases.

Tuesday, July 23

10:00 AM Richmond Fed manufacturing index, July (consensus -7, last -10)

10:00 AM Existing home sales, June (GS -4.1%, consensus -3.0%, last -0.7%)

Wednesday, July 24

08:30 AM Advance goods trade balance, June (GS -$103.0bn, consensus -$98.0bn, last -$99.4bn)

09:45 AM S&P Global US manufacturing PMI, July preliminary (consensus 51.7, last 51.6); S&P Global US services PMI, July preliminary (consensus 54.8, last 55.3)

10:00 AM New home sales, June (GS 632k, consensus 640k, last 619k)

04:05 PM Fed Governor Bowman and Dallas Fed President Logan (FOMC non-voter) speak: Fed Governor Michelle Bowman (via video) and Dallas Fed President Lorie Logan will give opening remarks at an event aimed at strengthening community partnerships in Dallas. Speech text is expected.

Thursday, July 25

08:30 AM GDP, Q2 advance (GS +2.3%, consensus +1.9%, last +1.4%); Personal consumption, Q2 advance (GS +2.3%, consensus +1.8%, last +1.5%); Core PCE inflation, Q2 advance (GS +2.79%, consensus +2.7%, last +3.7%): We estimate that GDP rose 2.3% annualized in the advance reading for Q2, following +1.4% annualized in Q1. Our forecast reflects strength in consumption (+2.3%, qoq ar) and nonresidential fixed investment (+4.3%), as well as a 1.2pp boost from inventory investment, that more than offset a decline in residential investment (-4.8%) and a 1.4pp drag from net exports. We also estimate that the core PCE price index increased 2.79% annualized (or 2.65% year-over-year) in Q2.

08:30 AM Durable goods orders, June preliminary (GS +0.2%, consensus +0.5%, last +0.1%); Durable goods orders ex-transportation, June preliminary (GS +0.4%, consensus +0.2%, last -0.1%); Core capital goods orders, June preliminary (GS +0.4%, consensus +0.2%, last -0.6%); Core capital goods shipments, June preliminary (GS +0.4%, consensus +0.2%, last -0.6%): We estimate that durable goods orders increased 0.2% in the preliminary June report (mom sa), partly reflecting seasonally soft commercial aircraft orders. We forecast firmer increases in the core measures, including 0.4% increases in both core capital goods shipments and core capital goods orders, based on solid US and foreign manufacturing activity.

08:30 AM Initial jobless claims, week ended July 20 (GS 235k, consensus 238k, last 243k); Continuing jobless claims, week ended July 13 (consensus 1,861k, last 1,867k)

11:00 AM Kansas City Fed manufacturing index, July (consensus -5, last -8)

Friday, July 26

08:30 AM Personal income, June (GS +0.45%, consensus +0.4%, last +0.5%); Personal spending, June (GS +0.25%, consensus +0.3%, last +0.2%); PCE price index, June (GS +0.10%, consensus flat, last flat); PCE price index (yoy), June (GS +2.49%, consensus +2.4%, last +2.6%); Core PCE price index, June (GS +0.20%, consensus +0.1%, last +0.1%); Core PCE price index (yoy), June (GS +2.60%, consensus +2.5%, last +2.6%): We estimate personal income increased 0.45% and personal spending increased 0.25% in June. We estimate that the core PCE price index rose +0.20%, corresponding to a year-over-year rate of 2.60%. Additionally, we expect that the headline PCE price index increased by 0.10% from the prior month, corresponding to a year-over-year rate of 2.49%. Our forecast is consistent with a 0.14% increase in our trimmed core PCE measure (vs. +0.09% in May and +0.21% in April).

10:00 AM University of Michigan consumer sentiment, July final (GS 65.7, consensus 66.4, last 66.0): University of Michigan 5-10-year inflation expectations, July final (GS 2.9%, last 2.9%)

Source: DB, Goldman

Tyler Durden

Mon, 07/22/2024 – 10:25

Share This Article

Choose Your Platform: Facebook Twitter Linkedin