More Guns, Less Butter: How Will The EU Wed Austerity To Militarization?

Authored by Conor Gallagher via NakedCapitalism.com,

US President Joe Biden, long showing signs of decline, is now officially done for in five months time, if not sooner. The current odds-on favorite to be the next president speaks often about turning away from Europe. Governments are collapsing, and countries are fracturing across the EU. And the eurozone economy is a mess.

{kind=link}

One might be tempted to come to the conclusion that it is time for the EU to start figuring out an exit strategy from its war against Russia. Trouble is, if the bloc’s crop of leaders were able to grasp the situation and act, they likely would have gotten out a long time ago – or never been game at all. Instead they kept digging deeper, and here again we have the EU doubling down.

EU diplomats have spent the past few weeks throwing a fit over Hungarian Prime Minister Viktor Orbán’s shuttle diplomacy efforts. In its very first session the newly elected Parliament produced a belligerent joint text, making all sorts of hardline demands, such as the removal of any restrictions on the Ukrainian use of Western weapons systems to strike Russian territory.

They also chose to reappoint one of the war’s biggest backers, Ursula von der Leyen, as president of the European Commission – the most powerful position in the EU. Let’s take a look at von der Leyen’s pitch as she worked to cobble together enough votes for her second five-year term and what the plan is now that she’s back. Emboldened by her reappointment, she is pushing for a defense union.

Politico describes this task as “the number one challenge of her second term: making huge amounts of EU money available to reindustrialize and re-arm the EU.”

Left unexplained is who would foot the bill for the ambitious plans, but the Commission and the European Central Bank continue to consider the possibility of issuing Eurobonds to finance the purchase or manufacture of weaponry, an idea considered off-limits until recently. Some background on the potential “miracle” of Euro defense bonds from Euractiv:

This miracle happened during the eurozone crisis when the EU created a legal instrument, the European Financial Stability Facility, able to issue bonds and with a lending capacity of €440 billion. And with the COVID pandemic, the miracle was repeated as the EU adopted a recovery fund with a firepower of €750 billion, financed through common debt issuance.

The same line of thinking has inspired politicians to imagine defence bonds – to finance a major boost of the EU’s defence capabilities, after years of neglect when it was assumed that war was a thing of the past or that Uncle Sam would always come to the EU’s defence.

Estonia’s Prime Minister [now the High Representative of the European Union for Foreign Affairs and Security Policy] Kaja Kallas highlighted in December the need for EU defence bonds to fight Russia’s aggression in Ukraine…

Speaking at the European Defence Agency annual conference on 30 November, [European Council President Charles] Michel said EU member states should pool what could amount to €600 billion in defence investment over the next 10 years.

He also said European defence bonds would be an attractive asset class, including for retail investors. Incidentally, a top European Investment Bank cautioned in an interview with Euractiv in January that investors don’t currently have an appetite for defence-related financial assets.

A couple of weeks later, French President Emmanuel Macron returned to the topic, telling investors at the World Economic Forum in Davos that Europe should resort to joint debt to finance its priorities, including defence.

Who doesn’t love “miracles?” But there are some issues, including economic difficulties across the bloc, governments crumbling, and public frustration with everything from the immigration to the economy. There is also the reported military manpower shortages, which is a whole other problem that has been frequently covered.

Politico quotes an unnamed diplomat who says that “Everything that costs anything — for example, Ukraine defense,” will prove “problematic” during von der Leyen’s second term. While von der Leyen is throwing around figures like 500 billion over the next decade, another diplomat said, “We didn’t see spreadsheets, we didn’t see details, this is pie in the sky money.”

More details are likely coming soon as von der Leyen is planning to appoint a Commissioner for Defense who will present a white paper on the future of European militarization efforts within 100 days.

The real question is whether Germany will go along with any eurobond plan. The historically unpopular chancellor Olaf Scholz remains opposed to Euro defense bonds – for now. He argues that the EU already has various research and industrial funds to support defense cooperation among member states and defense companies.

For example, Poland, France, Germany and Italy just signed a letter of intent to jointly develop long-range cruise missiles. Poland and Germany were among those countries that got rid of their missiles in the 1990s following the 1987 Intermediate-Range Nuclear Forces Treaty. That agreement expired in 2019, however, after then-president Donald Trump withdrew from it. The US is ever-so-generously agreeing to cover Germany where US long-range missiles will be rotationally deployed in 2026 as a temporary solution.

While Scholz talks up agreements like the joint development of long-range cruise missiles, Atlanticists are insisting he do more, and he does not have a strong record of firmness when pressured by his NATO/EU colleagues.

Recall in the Fall of 2022 when he resisted sending more heavy arms to Ukraine. After a few weeks of badgering, he pledged to support Ukraine “for as long as it takes.” He also caved on the Leopard tanks after making a show of resistance. On the other hand, the Taurus missiles still haven’t been sent to Ukraine. Yet the Eurobond issue is starting to be reminiscent of these previous pressure campaigns. It was only four months ago that idea was viewed as “radical;” now Germany is viewed as the main roadblock.

Berlin is facing its own budgetary constraints while also pushing arbitrary limits onto other EU nations, and the inadequate ramp up of military spending is “set[ting] the stage for further clashes with Germany’s international partners, especially Washington, in the coming months.” On the other hand, any eurobond plan would only strengthen political threats to the “center” in Germany, such as the Alternative for Germany and Sahra Wagenknecht who want to stop the digging and attempt to repair ties with Russia.

Could a Trump Election Further Von Der Leyen’s Goals?

It’s important to note that Trump didn’t actually undermine the NATO alliance in any significant way as president and appointed CIA officials and neocons to run his hawkish foreign policy, although there is hope that will change in a second go-round.

In reality, however, the plan for the US to take a backseat on the European front and focus on the Pacific is part of a strategy long pushed by neocons. It might be an unrealistic and dangerous one, but it is a strategy nonetheless. Here is a team from the influential Center for Strategic and International Studies (CSIS) writing earlier this year in Foreign Affairs about how Europe must lead in the fight against Russia so the US can focus on China:

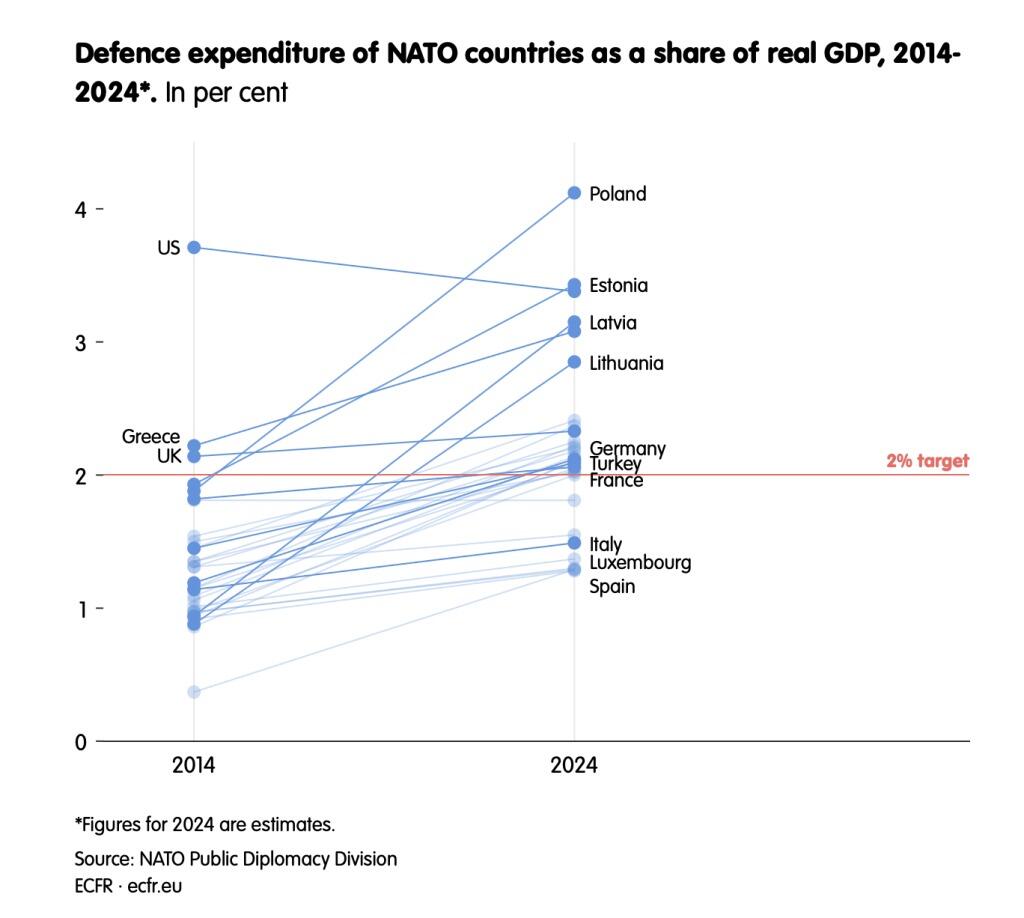

That complicated reality requires U.S. allies, especially in Europe, to take on a larger share of directing the containment of Russia. Europe has shown its political and economic resilience in the face of Russian aggression. Yet militarily, the continent remains dependent on the United States. This dynamic must change, in part because the United States must commit more of its resources to Asia. The growth of European defense spending since Russia’s full-scale invasion of Ukraine is an encouraging step. In 2023, 11 NATO members hit their spending target, allocating at least two percent of GDP to national defense, up from just seven members in 2022. The rest need to follow suit.

Europe must also resolve the problem of coordination. Right now, the United States coordinates more than 25 militaries in Europe. While it must continue to do this in the short term, it must push individual European countries and the European Union to take over this role and to create a stronger European pillar in NATO.

This is precisely what is atop Queen Ursula’s to-do list for her second term, so a second Trump presidency might not be a disaster but an opportunity in the eyes of ambitious and deluded in Brussels who want to amass more power in the name of marshaling the bloc’s finances to ramp up militarization efforts against the Russian menace.

In many ways Europe’s bureaucracy has already changed in small but fundamental ways in order to redirect money towards war. From Equal Times:

“In 2023, there was a very significant increase in military spending worldwide, but especially in Europe. In Spain, for example, it grew by 24 per cent and in Finland by 36 per cent. If we compare it with 2013, the European countries in Nato are spending 30 per cent more,” says Pere Ortega, a researcher at the Barcelona-based Centre Delàs for Peace Studies, which is critical of measures adopted by the European Commission to promote military spending, such as the VAT exemption for the purchase of armaments or the change in the regulations of the European Investment Bank (EIB) to allow it to finance industrial projects in the military sphere.

And according to the European Council on Foreign Relations (ECFR), the number of countries meeting the two percent target has risen from 3 to 23 since 2014:

{kind=link}

The problem now is that individual states are running into budgetary constraints.

More Guns, Less Butter

EU leaders are determined to reimpose austerity on bloc countries beginning in 2025. That’s a return to the annual limits of 3 percent of GDP for public deficits and 60 percent for public debt, which were suspended in response to the Covid-19 pandemic.

There are some new twists to the rules that were marketed as measures to soften the pain, but if they do, it will be minimal. For example, the new agreement stipulates that countries with a deficit above 3 percent of GDP are required to halve this to 1.5 percent but can do so during periods of growth. That growth might quickly evaporate with such a public spending pullback, but that’s the plan. Elsewhere, countries will still be required to reduce their debt on average by 1 percent per year if it is above 90 percent of GDP, and by 0.5 percent per year on average if the debt is between 60 percent and 90 percent of GDP. The new rules give countries seven years to get their spending in order, up from four previously.

These rules will make it close to impossible to spend more on defense without completely cutting social services to the bone. Even without factoring in increased defense expenditures the outlook is grim:

Too meet reformed EU fiscal rules, Italy and France would have to go for fiscal consolidations over 2025-2028 that are larger than during the Euro Crisis (2011-2014). Spain has to do about half.

Do we properly remember the effects and political debates of €zone austerity? pic.twitter.com/Rmuz8jfkTJ

— Philipp Heimberger (@heimbergecon) June 21, 2024

So how to reconcile the goal of a defense union and remilitarization with plans for austerity?

A few possibilities:

There is talk of exemptions from the debt rules for military spending.

Bloomberg reported back in March that EU officials and investors are using the fiscal rules to push for an EU-wide bond program that would bring the investors bigtime profits while allowing the bloc to ramp up military spending without individual nations incurring more debt.

Of course a third option is that the EU will abandon its war against Russia, stop supporting Nazis, quit fetishizing austerity, and rebuild its economies, but back to reality.

The big question remains if Germany will get onboard with the EU bond program. One reason it could is because it would help Berlin with its own budgetary constraints. While Germany wouldn’t face major budget crunches like France, Italy, and Spain under the return of debt and deficit rules, it is hamstrung by its self-imposed deficit brake.

That rule, intended to force German governments to balance the federal budget, was introduced under former Chancellor Angela Merkel during the euro crisis and restricts deficit spending to a minimum, except under “extraordinary” circumstances, such as a natural disaster or war. The current government tried to override the brake in order to shovel more money into the Ukraine bottomless pit, but was rebuked last Fall by the constitutional court.

An EU-wide war bond program could help the bloc bypass all the self-imposed debt brakes while still cutting and privatizing social services, and both could be a boon for investors. What’s not to love? The Centre for European Policy Studies with more:

Against this backdrop, the EU’s true ‘Hamiltonian moment’ in defence would be a decision to issue joint debt to properly fund the ambitions set out in its Defence Industrial Strategy.

Based on Art. 122 TFEU and implemented in accordance with Articles 173-174 TFEU, such bonds—possible under the EU’s Financial Regulation—could provide the backbone for grants to Member States to bolster the Union’s defence production capacity if paired with existing incentives for joint capabilities research, development, production, and procurement. This would avoid the two-speed logic and weaker conditionalities surrounding proposals to use the European Stability Mechanism (excluding key countries such as Poland, Sweden and Denmark) to issue loans to EU Member States for defence spending.

Like how the Covid-induced Recovery and Resilience Facility stabilised European markets and sustained demand during and after the pandemic, Euro-defence bonds are a potential game-changer for the EU’s defence ambitions due to the potential speed and scale of resource mobilisation, and the potential impact on market de-fragmentation. And, fortunately, the German Constitutional Court should have nothing to object to this time around.

The View from Outside the Cult

Voices from Moscow, Budapest, and Belgrade are issuing warnings that the EU continuing down this road increases the threat of war, and they are concluding that is what Brussels wants.

Moscow is taking note of von der Leyen’s plans and preparing accordingly according to Kremlin spokesman Dmitry Peskov:

“[It] confirms the general attitude of European states to militarisation, escalation of tension, confrontation and reliance on confrontational methods in their foreign policy,” said Peskov “Everything is quite obvious here.”

The Kremlin spokesman added that while Russia did not pose a threat to the EU, actions by its member states regarding Ukraine “have excluded any possibility of dialogue and consideration of Russia’s concerns. These are the realities in which we have to live, and this forces us to configure our foreign policy approaches accordingly,” Peskov said.

Hungarian Prime Minister Viktor Orban, childishly reprimanded by the EU for talking peace with world leaders, keeps warning about the levels of delusion in Brussels. His latest in a Magyar Nemzet op-ed:

The Brussels bureaucrats want this war, they see it as their own, and they want to defeat Russia. They keep sending the money of the European people to Ukraine, they have shot European companies in the foot with sanctions, they have driven up inflation and they have made making a living difficult for millions of European citizens.

Serbian President Aleksandar Vucic echoed those thoughts in a recent interview with the Pink TV channel:

“The West would like to conduct warfare from a distance, through someone else, through investing money and so on, but at the moment they are not ready [for a direct conflict with Russia]. Will they be ready? They are not ready now, but I think they will be ready. They are already preparing for a conflict with the Russian Federation and they are preparing much faster than some people would like to see, in every sense. We know that from the military preparations, we know how they’re going. And I want to tell you, they are preparing for a military conflict.”

Tyler Durden

Thu, 07/25/2024 – 06:30

Share This Article

Choose Your Platform: Facebook Twitter Linkedin