Treasury Trims Debt Estimates For Current Quarter, But Q1 Borrowing Surge To Follow

Back in July and exactly one quarter ago, when the US Treasury published its debt issuance forecast for the balance of 2024, we said that the “anticipated numbers came close to our estimates for Q3, but well above our forecast for Q4” with the highlight being the Q4 debt issuance number which the Treasury estimated at $565 billion, $115 billion above our estimate of $450 billion (in part due to the Treasury higher TGA estimate of $700 billion vs our assumption of $650 billion).

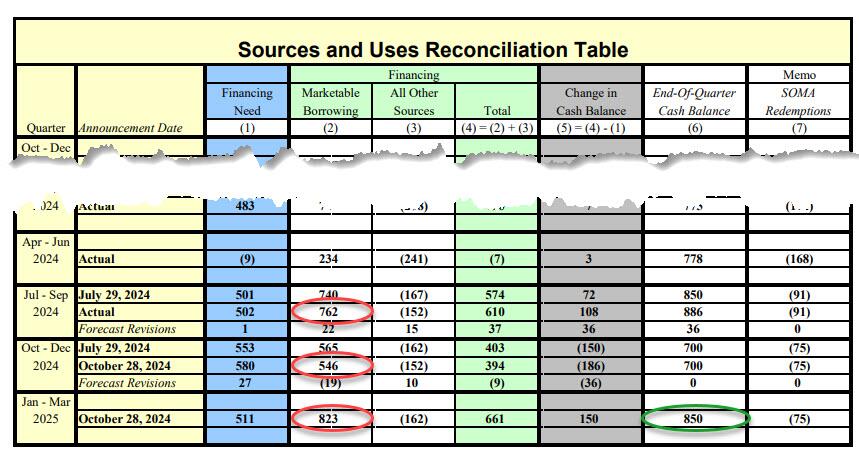

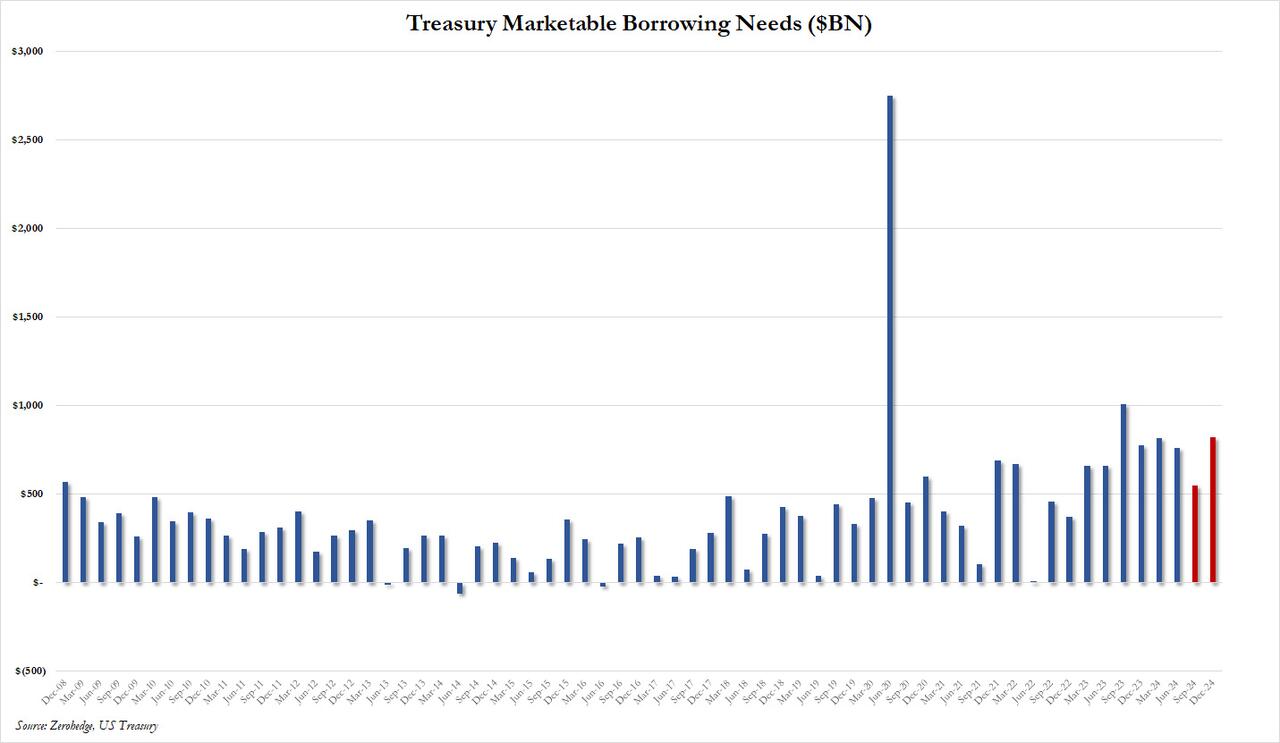

Fast forward to today when ahead of Wednesday’s Quarterly Refunding Announcement, at 3pm ET the Treasury published its debt sources and uses forecast for the current and coming quarters, and it showed that the Treasury trimmed its estimate for borrowing for the current quarter, while raising more debt than it previously expected in the quarter ended June 30; The Terasury also continues to expect a $700 billion cash balance at the end of the year, just before the federal debt ceiling kicks back in. Then as we enter 2025, the Treasury expects to raise $823 billion in new debt in the first calendar quarter of 2025, in large part because it expects that the Treasury cash balance will rise by $150 billion to $850 billion, or in other words, the Treasury does not assume another debt ceiling crisis which would push the cash balance sharply lower in Q1 and onward.

Here are the details from the Treasury statement:

During the July – September 2024 quarter, Treasury borrowed $762 billion in privately-held net marketable debt and ended the quarter with a cash balance of $886 billion, more than the $850 billion initially expected. In July 2024, Treasury estimated borrowing of $740 billion and assumed an end-of-September cash balance of $850 billion. Privately-held net marketable borrowing was $22 billion higher largely because of a $36 billion higher ending cash balance partially offset by higher net cash flows.

During the October – December 2024 quarter, Treasury expects to borrow $546 billion in privately-held net marketable debt, assuming an end-of-December cash balance of $700 billion. The borrowing estimate is $19 billion lower than announced in July 2024, largely due to a higher beginning-of-quarter cash balance partially offset by lower net cash flows.

{kind=link}

During the January – March 2025 quarter, Treasury expects to borrow $823 billion in privately-held net marketable debt, assuming an end-of-March cash balance of $850 billion. Of note,the end-of-March cash balance assumes another successful “enactment of a debt limit suspension or increase” which, assuming Trump becomes president, is virtually guaranteed will not happen. Indeed, should we get another debt ceiling crisis, the Treasury is quick to note that while the debt limit is not currently binding, “Treasury’s cash balance may be lower than assumed depending on several factors, including constraints related to the debt limit.” Translation: Q1 cash balances will be sharply lower than expected since the odds of a successful debt ceiling renegotiation are slim to none if Trump wins next week.

Here is the debt schedule in table format:

{kind=link}

Dealers’ expectations for the new borrowing estimate had varied ahead of Monday’s release. Strategists at JPMorgan Chase & Co. expected a cut to $529 billion. But the team at BNP Paribas predicted an increase to $600 billion, based in part on October and November making up nearly a quarter of the federal government’s annual deficit, a gap that has been steadily widening.

Meanwhile, the projected $823 billion borrowing need in Q1 2025 would be the highest since the Sept 2023 quarter.

{kind=link}

“We estimate that the Treasury will begin to limit bill supply in March 2025 and will cut bill supply aggressively in Q2,” a team of strategists a TD Securities including Gennadiy Goldberg wrote in a note, which would be expected since by then the Reverse Repo buffer will be all used up. Before then, however, the TD team said that “with a debt ceiling increase or suspension likely in Q3, Treasury will then ramp up bill issuance aggressively as the cash balance is rebuilt to a more normal level.”

{kind=link}

Wrightson ICAP economist Lou Crandall didn’t expect officials this week to provide any color on their specific expectations for the upcoming debt ceiling timeline. He had predicted a $540 billion October-through-December borrowing estimate ahead of Monday’s release.

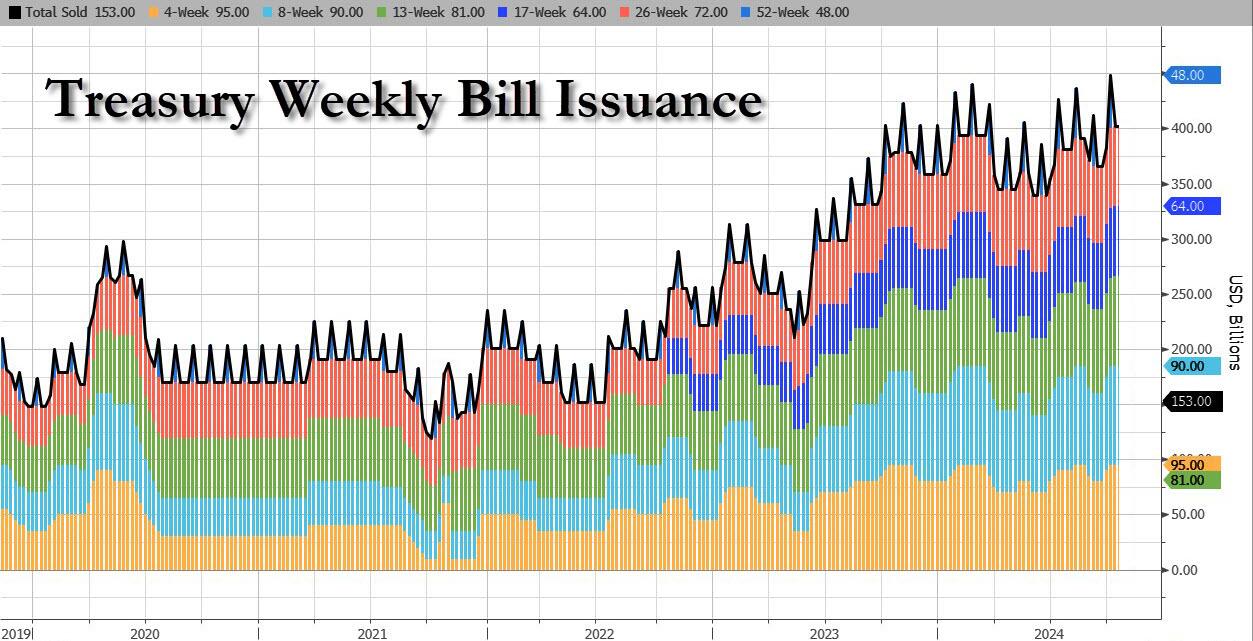

Today’s report comes ahead of Wednesday’s quarterly refunding announcement, when the Treasury will unveil its plans for long-term debt issuance. Bond dealers widely expect that the refunding auctions will total $125 billion for the third straight quarter. Many also expect a ramp up in Bill Issuance in the tail end of the year, which would be a big problem at a time when the Reverse Repo facility only holds just over $200 billion, and is in danger of being rapidly depleted, sparking another repo market crisis.

Tyler Durden

Mon, 10/28/2024 – 15:48

Share This Article

Choose Your Platform: Facebook Twitter Linkedin