Beware Of A Market Trading At All-Time Highs

Authored by Jan-Patrick Barnert via Bloomberg,

The tricky thing about markets at all-time highs is that they can easily flip. And what currently looks like a bit of a sideways consolidation has all the ingredients to make things messy in the next few weeks.

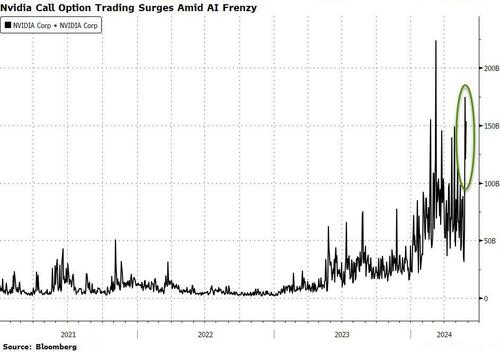

Take the seemingly endless risk appetite for all things artificial intelligence, epitomized by the explosion higher in Nvidia shares after Musk headlines sparked an options gamma squeeze. We can argue all day about the fair value of the leading AI chip maker, but the rally has the potential to keep risk taking, especially from retail, on a relatively high level almost regardless of fundamentals.

{kind=link}

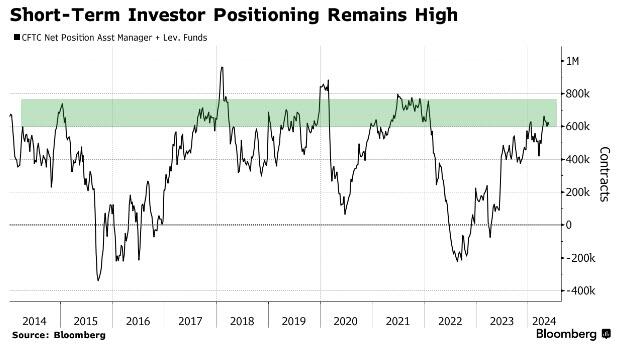

Hedge funds’ exposure to the so-called Magnificent Seven companies is at a record high since Nvidia Corp.’s estimate-beating earnings last week, according to Goldman Sachs’s prime brokerage. The firms now accounts for almost 21% of hedge funds’ total net exposure to US single stocks. Supportive? Yes. High risk of profit taking and stops being triggered? Also yes.

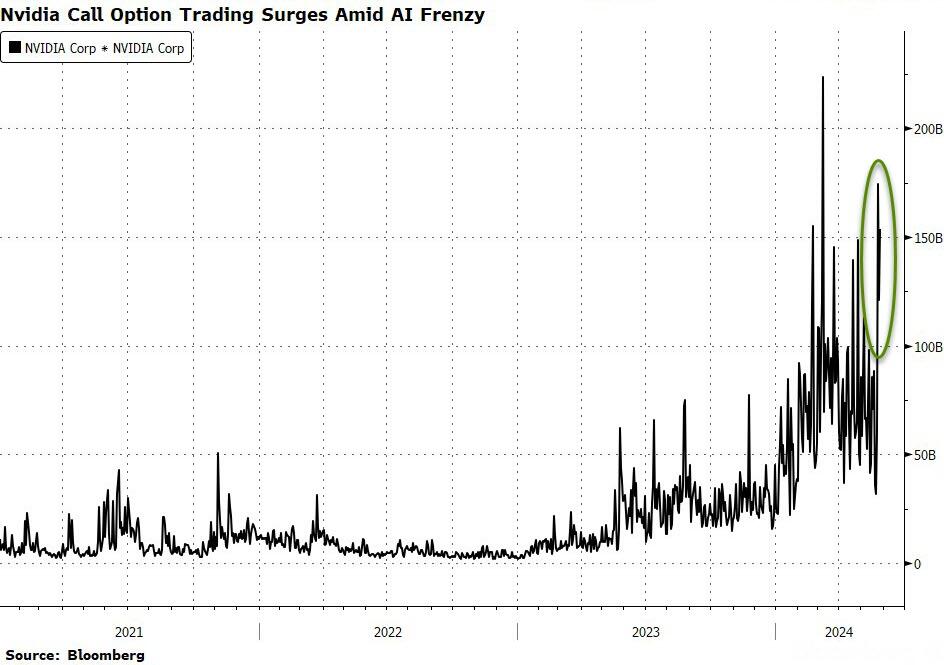

Then there’s rates, another major sentiment building block that’s looking wobbly again. European stocks fell for a second day and bonds retreated, tracking a drop in US Treasuries overnight. US 10-year yields have smashed through 4.5% after weak debt auctions and hawkish remarks from a Federal Reserve speaker. And while stocks were mostly ignoring a rise in bond yields since mid-May it seems that once again the overflow container for rate concerns is at maximum capacity and stocks can’t ignore the issue any longer.

{kind=link}

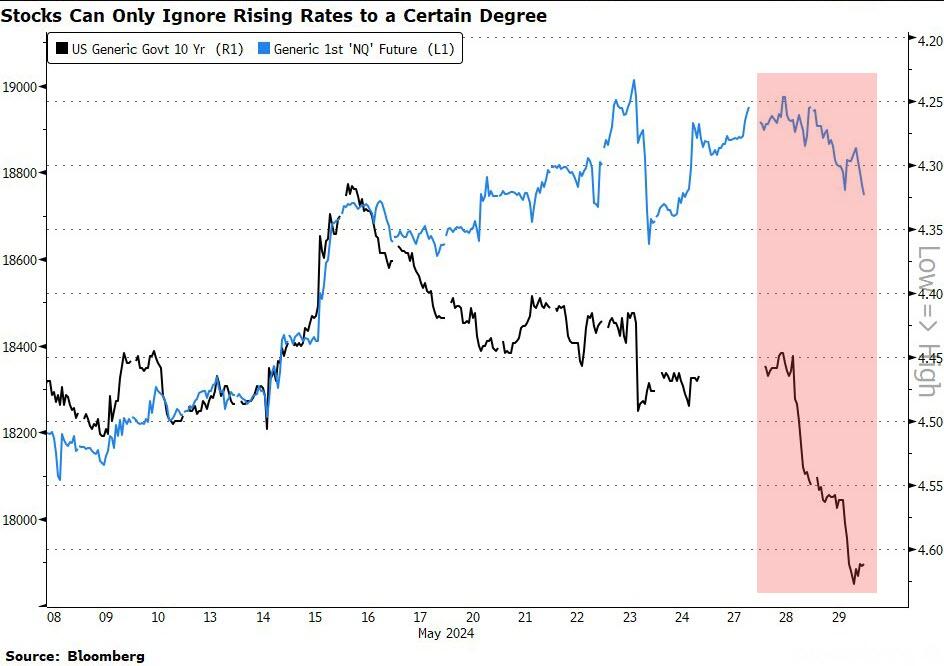

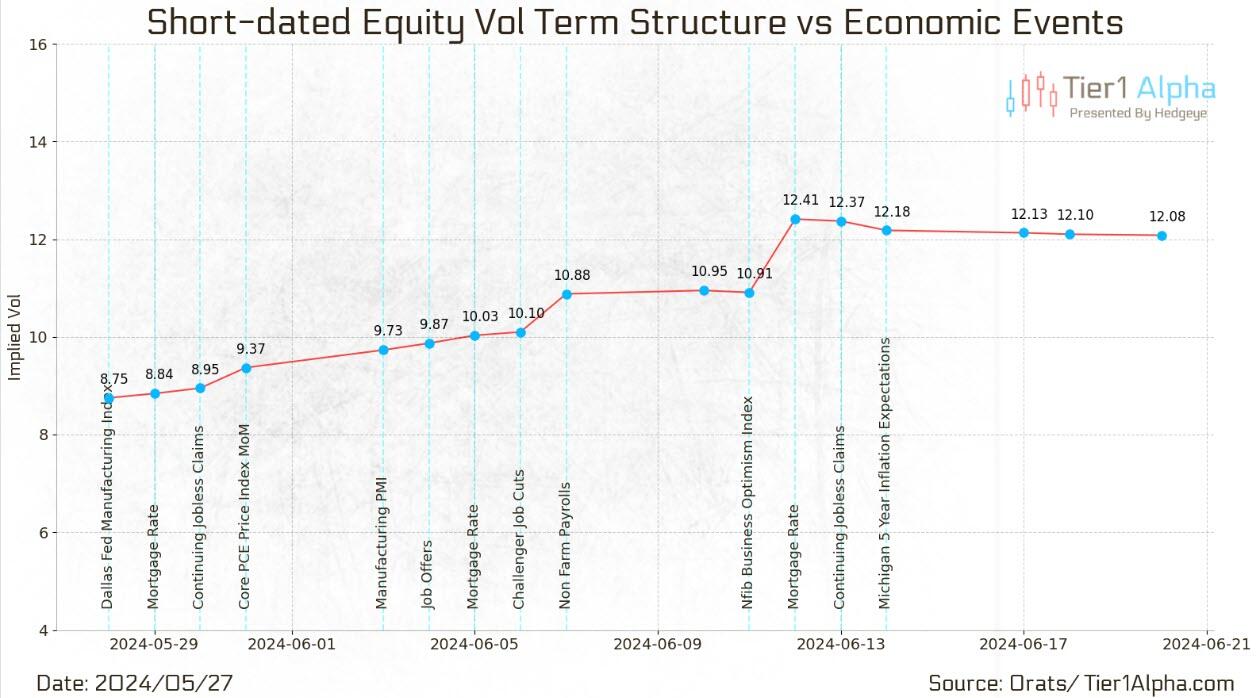

The move is awakening the sleepy volatility readings and shows that markets, while still very calm, are mindful of the path of inflation and rates. Wording from central banks seems to increase in weight when it comes to describing not just the timing of the first cut but also the path beyond it. And while demand for hedges is still rather low, the rise in skew is a key measure many are watching when it comes to determining if markets reach a conditional state of increased downside risks.

{kind=link}

Systematic investors are once again in a state where their influence on stocks is very asymmetric. Goldman Sachs traders predict that CTA funds have to buy about $4 billion in stocks over the next month both in a flat or up market. That stands in contrast to $217 billion of selling should the market decline.

“High positioning and low volatility feel complacent, but may continue into summer and fuel systematic buying,” notes Emmanuel Cau, a strategist at Barclays, adding that both fundamentals and share buybacks are still a boost to equity demand.

{kind=link}

As low-volatility seasonal patterns are upon us, the strategist expects equity volatility to persist at extremely depressed levels. That said, investors might want to make use of it again, not just to buy hedges but to play the upside as well. “We like using extremely low cost of optionality for equity replacement by buying calls or call spreads instead of being outright long equities,” Cau says.

Still, the super low volatility backdrop, despite macro risk events such as the US GDP release and inflation data out of Europe, is a bit of a head scratcher, especially as the economic surprise index is deteriorating and making the elevated stock market more vulnerable.

It raises the risk that the “unhedged pot may indeed boil,” write the strategists at Tier 1 Alpha. They add that the risk is higher than normal given dealers’ option positioning and a put/call skew across multiple tenors that suggests a modest increase in downside protection demand.

{kind=link}

Tyler Durden

Thu, 05/30/2024 – 10:15

Share This Article

Choose Your Platform: Facebook Twitter Linkedin