China Ramps Up Warning On Bond-Buying Frenzy With PBOC Selling in Focus

By John Liu and Zheng Wu, Bloomberg Markets Live reporters and strategists

Three things we learned last week:

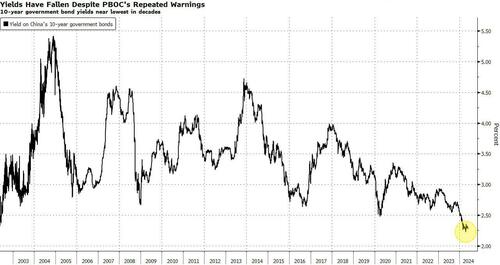

1. China’s central bank gave its strongest warning yet against overheating in the government bond market. A paper backed by the People’s Bank of China said the monetary authority is ready to sell bonds if needed and suggested a reasonable range for the 10-year yield should be 2.5% to 3%.

PBOC’s repeated warnings against what it deems as excessively low yields have largely been shrugged off by investors. Unconvinced by China’s economic recovery and housing rescue plans, bond bulls have been betting the central bank will have to do more, such as lowering interest rates and even turning to the controversial step of quantitative easing.

{kind=link}

Investors may have to take it more seriously this time. The PBOC has every reason to be concerned over falling interest rates. While cheaper borrowing costs have benefits, a yawning yield gap with the US is adding pressure on the yuan and fueling bearish sentiment toward Chinese assets — raising the risk of capital outflows.

The central bank may want to root out expectations of aggressive monetary easing. Such speculations have led to an influx of money into the bond market, draining bank deposits and funds available for the real economy. It may perhaps be sending a subtle message to the Ministry of Finance that the the heavy-lifting of growth should come from the fiscal side.

2. China’s factory activity unexpectedly contracted with the official manufacturing purchasing manager index falling to 49.5. While more focus was given to the sudden weakness, the non-manufacturing gauge also flashed a warning with a slower-than-expected expansion. Together, they put in doubt the ability of China to reach the growth target of around 5% this year.

China’s recovery this year has largely been driven by export-oriented firms as domestic consumption is weighed down by the real estate slump. That pillar of strength is at risk of losing its mojo as trade tensions rise along with more protectionist measures against Chinese products. Persistent demand weakness may also be starting to erode production strength, according to Citi analysts.

While stock market reaction was muted right after the PMI data release, key equity gauges ended Friday in the red while the yuan also slipped against the dollar. The weakness in eco data tends to draw mixed reaction among investors, with some seeing it as a positive signal for more policy support while others regard it as just another reason to sell Chinese assets.

3. Last week started with renewed excitement over property support as top-tier cities joined the easing bandwagon, but the upbeat mood didn’t last long. A Bloomberg Intelligence index tracking China’s developer stocks slid around 6% in the five days through Friday, taking its loss since a May 17 high to roughly 19%.

Shanghai, Shenzhen and Guangzhou lowered requirements for home downpayments and cut the minimum rates charged for mortgages, following through on the central government’s aid for the embattled property sector. The fact that property shares fell despite the easing measures from China’s biggest cities shows the bar to satisfy frustrated investors is getting higher and higher.

{kind=link}

The mood is more cautious among fixed-income managers, who pay closer attention to the developers’ credit risks. They say the sector is not out of the woods yet, with their refinancing options limited ahead of near-term maturity walls. As the chorus grows for even more policy support, it’s unclear how and when the property crisis can be solved. The country has the equivalent of 60 million unsold apartments, which will take more than four years to sell without government aid, according to Bloomberg Economics.

Tyler Durden

Sun, 06/02/2024 – 22:37

Share This Article

Choose Your Platform: Facebook Twitter Linkedin