Key Events This Week: Fed, CPI and PPI

With the (ridiculously manipulated propaganda) jobs report now in the history books, this week the whole financial world will be focused on Wednesday with two big events occurring: the latest FOMC and CPI (with PPI to follow on day later). Below, DB’s Jim Reid previews the first two below but other events this week include NY Fed 1-yr inflation expectations today, UK employment data, US small business optimism and a 10yr UST auction tomorrow, China CPI and Japanese PPI on Wednesday, waking up to a mid-life crisis on Thursday alongside US PPI and a 30yr UST auction, with the BoJ decision and the US UoM consumer sentiment on Friday.

{kind=link}

Before we delve deeper, it is fascinating to see the negative reaction of French bond markets this morning after the surprise news last night that Macron has called for snap legislative elections which will take place in two rounds on June 30th and July 7th. This is after his party trailed with 15% in the European Parliamentary (EP) elections with Le Pen’s National Rally (RN) winning 32%. Although this was broadly in line with expectations, Macron is likely hoping to win back some momentum and hope a notable part of the EP results were a protest vote and also encourage other centrist parties to help rally round to limit the charge of Le Pen. His other hope would be that if RN have a bigger part in government, their appeal may diminish before the next Presidential elections in 2027. So a big gamble.

In terms of the wider EP elections the main takeaway is that even with the uncomfortable results in France and Germany, the centrist majority is holding as the far-right didn’t outperform expectations in aggregate. As the results have started to materialise the Euro is -0.44% lower as I type, at 1.0753 against the dollar, its weakest level in nearly a month.

Moving forward, Reid previews the main events of the week in more detail now. According to the DB strategist, it’s not very often you have a US CPI released on the same day as a FOMC meeting and the former will certainly factor into the latest Fed Summary of Economic Projections (SEP). On Friday, a few US houses who were expecting summer Fed cuts pushed back their projections after the strong payroll number and this release will also influence the tone of the meeting. DB economists believe the new SEP forecasts are likely to revise core PCE inflation higher this year (2.8%), and move the median dot from three rate cuts to two with a desire for optionality for September perhaps the only thing preventing this moving nearer to DB’s long standing expectation of a cut only arriving in December. The DB econ team also expects the 2025 median dot to move up by 25bps as well and the long-run dot to 2.75% (with risks it moves even higher).

Powell’s press conference will no doubt offer nuances around any changes and will have the ability to put a dovish or hawkish spin on them. At this stage optionality will likely be preferred with little specific guidance.

May’s CPI release hours earlier will cast a long shadow over the meeting. The DB Econ team expects headline CPI (+0.12% forecast vs. +0.31% previously) to come in softer than core (+0.27% vs. +0.29%), helped by declining gas prices last month. This would reduce the core YoY rate by a tenth to 3.5%, with the headline remaining steady at 3.4% (in-line with consensus). Under these forecasts the three-month annualized core rate would fall three-tenths to 3.8%, while the six-month annualized rate would remain at 4.0%. Obviously as ever rents will get a lot of attention to see if they are falling as the models suggest they should be and then for PPI on Thursday, the components that feed directly into core PCE (namely health care services, domestic airfares, and portfolio management) will be the main thing to watch.

For the Fed to cut rates in September (unlikely in our eyes), or earlier (only in an imminent crisis), inflation must fall sharply, or employment needs to weaken considerably. For the latter, Friday’s payroll suggested that this will be tough to see in the data quickly enough. May’s headline (+272k) and private (+229k) payroll gains were well above the +180k and +165k expected respectively with a 0.4% gain in average hourly earnings a tenth higher than expected. The diffusion index (63.4) was the highest level since January 2023 which shows that job growth has broadened out after narrow gains for a lot of the last year.

The other two big events of the week are the Chinese inflation and the BoJ. For the former, current median estimates on Bloomberg suggest the CPI may improve to +0.4% YoY in May from +0.3% in April, with the PPI also coming in higher relative to the previous reading (-1.5% vs -2.5% in April). For the latter, economists expect the target short-term interest rate to remain unchanged but highlights that the focus will be on guidance for JGB purchases. They also see changes including a reduction of the central bank’s purchases from the current 6tn yen per month to 5tn yen.

Courtesy of DB, here is a day-by-day calendar of events

Monday June 10

Data : US May NY Fed 1-yr inflation expectations, Japan May bank lending, Economy Watchers survey, April BoP current account balance, BoP trade balance, Italy April industrial production, Sweden April GDP, Norway and Denmark May CPI

Central banks : ECB’s Holzmann speaks

Auctions : US 3-yr Notes ($58bn)

Tuesday June 11

Data : US May NFIB small business optimism, UK April average weekly earnings, unemployment rate, May jobless claims change, Japan May M2, M3, machine tool orders, Canada April building permits

Central banks : ECB’s Villeroy, Rehn, Holzmann and Lane speak

Earnings : Oracle, GameStop

Auctions : US 10-yr Notes (reopening, $39bn)

Wednesday June 12

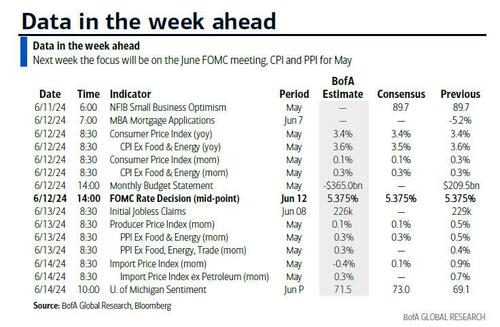

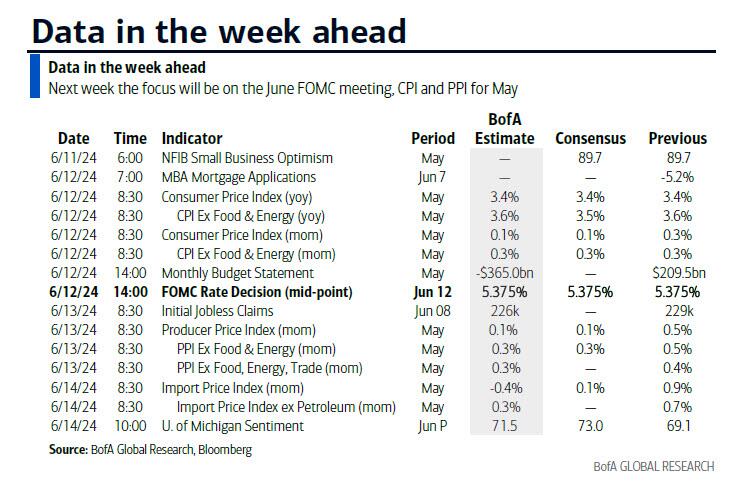

Data : US May CPI, monthly budget statement, China May CPI, PPI, UK April monthly GDP, Japan May PPI, Germany April current account balance

Central banks : Fed’s decision, ECB’s Guindos speaks

Earnings : Broadcom

Thursday June 13

Data : US May PPI, initial jobless claims, UK May RICS house price balance, Germany May wholesale price index, Italy Q1 unemployment rate, Eurozone April industrial production

Central banks : Fed’s Williams interviews US Treasury Secretary Yellen

Earnings : Adobe, Wise

Auctions : US 30-yr Bond (reopening, $22bn)

Friday June 14

Data : US June University of Michigan survey, May import and export price indices, Japan April Tertiary industry index, capacity utilisation, Italy April trade balance, general government debt, Eurozone April trade balance, Canada April manufacturing sales, Sweden May CPI

Central banks : BoJ decision, Fed’s Goolsbee speaks, ECB’s Lagarde, Lane and Vasle speak, BoE’s inflation attitudes survey

Finally, focusing on just the US, Goldman notes that the key economic data releases this week are the CPI report on Wednesday and the PPI report on Thursday. The June FOMC meeting is on Wednesday. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM.

Monday, June 10

11:00 AM New York Fed 1-year inflation expectations, May (last 3.26%)

Tuesday, June 11

06:00 AM NFIB small business optimism, May (consensus 89.6, last 89.7)

Wednesday, June 12

08:30 AM CPI (mom), May (GS +0.11%, consensus +0.1%, last +0.3%); Core CPI (mom), May (GS +0.25%, consensus +0.3%, last +0.3%); CPI (yoy), May (GS +3.36%, consensus +3.4%, last +3.4%); Core CPI (yoy), May (GS +3.50%, consensus +3.5%, last +3.6%): We estimate a 0.25% increase in May core CPI (mom sa), the softest sequential pace since October. Our forecast reflects a 3% pullback in airfares and price weakness across consumer products, as indicated by Adobe online price data and consistent with Target’s announced price cuts. We also forecast a deceleration in car insurance rates (+1.0% vs. +1.8% in April) based on online price data. We assume another decline in new car prices (-0.3%) but a 1.1% rebound in the used car measure. We estimate stable inflation in the housing measures (primary rent +0.35%; OER +0.42%). We estimate a 0.11% rise in headline CPI, reflecting lower energy (-1.4%) and unchanged food prices. Our forecast composition is consistent with a 19bp increase in core PCE in May (mom sa).

02:00 PM FOMC statement, June 11-12 meeting: As discussed in our FOMC preview, we continue to expect the first rate cut in September, by which point we expect to have seen five straight months of better inflation news. After September, we expect quarterly rate cuts to a terminal rate of 3.25-3.5%. This implies a second cut in December for a total of two cuts in 2024, four more in 2025, and two more in 2026. At the June meeting, we expect the median forecast of 2024 Q4/Q4 core PCE inflation to rise 0.2pp to 2.8%. The GDP growth and unemployment rate projections should be little changed. We do not expect any significant changes to the FOMC statement or Chair Powell’s message. We expect the median forecast in the dot plot to show two cuts in 2024 (vs. three in March) to 4.875%, four cuts in 2025 (vs. three in March) to 3.875%, and three cuts in 2026 (unchanged) to 3.125%.

Thursday, June 13

08:30 AM Initial jobless claims, week ended June 8 (GS 225k, consensus 220k, last 229k): Continuing jobless claims, week ended June 1 (last 1,792k)

08:30 AM PPI final demand, May (GS +0.1%, consensus +0.1%, last +0.5%); PPI ex-food and energy, May (GS +0.3%, consensus +0.3%, last +0.5%); PPI ex-food, energy, and trade, May (GS +0.3%, last +0.4%)

12:00 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will moderate a discussion with Treasury Secretary Janet Yellen at an event hosted by the Economic Club of New York. A Q&A is expected. On May 30, Williams said, “I see the current stance of monetary policy as being well positioned to continue the progress we’ve made toward achieving our objectives… Looking at the broader context, the behavior of the economy over the past year provides ample evidence that monetary policy is restrictive in a way that helps us achieve our goals.” He added, “I expect overall PCE inflation to moderate to about 2½ percent this year, before moving closer to 2 percent next year… Overall, I see some of the recent inflation readings as representing mostly a reversal of the unusually low readings of the second half of last year, rather than a break in the overall downward direction of inflation.”

Friday, June 14

08:30 AM Import price index, May (consensus +0.1%, last +0.9%): Export price index, May (consensus +0.1%, last +0.5%)

10:00 AM University of Michigan consumer sentiment, June preliminary (GS 72.7, consensus 73.0, last 69.1): University of Michigan 5-10-year inflation expectations, June preliminary (GS 3.0%, consensus 3.0%, last 3.0%)

02:00 PM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will speak in a fireside chat at the Iowa Farm Bureau Economic Summit. A Q&A is expected. On May 10, Goolsbee said, “There isn’t at this time much evidence, in my view, that inflation is stalling out at 3%…we hit this bump [in Q1] and now I think we wait…I still don’t accept that we’re stuck at the last mile and that’s going to be the hardest. That’s one of the things we’re trying to determine – are we hung up at a higher level of inflation, which is what the last two and a half months say, or is that just a bump, which is what the previous seven months say?” He added, “If r-star is increasing, and maybe it is, why [is it increasing]?…My objection with the arguments that maybe r-star is changing is none of those empirical data contributions that would raise r-star have changed in the last six months.”

07:00 PM Fed Governor Cook speaks: Fed Governor Lisa Cook will give remarks on lessons from the American Economic Association Summer Program. Speech text is expected but a Q&A is not.

Source: DB, Goldman, BofA

Tyler Durden

Mon, 06/10/2024 – 09:40

Share This Article

Choose Your Platform: Facebook Twitter Linkedin