Stocks Slide, Bonds Bid As Crude Crumbles

After a promising start to the overnight session, which saw both Asia and Europe perk up to start the new month alongside a furious surge in GameStop on the latest meme stonk shenanigans by Roaring Kitty, the mood deteriorated rapidly, and after a very ugly, and quite stagflationary Mfg ISM print, which printed below the lowest estimate (and just as ugly Construction Spending print to boot), the hard landing trade re-emerged, and “bad news was once again bad news” as both yields.

{kind=link}

“Bad news may no longer be good news,” said Jose Torres at Interactive Brokers, who was quoted by Bloomberg.

Torres continued, “In recent months, investors have cheered weaker-than-estimated data based on expectations that it could accelerate the start of the Fed’s policy loosening. Investors are now reacting to soft data with fear.”

Yields across the Treasury curve continued their decline from late last week into the new week.

{kind=link}

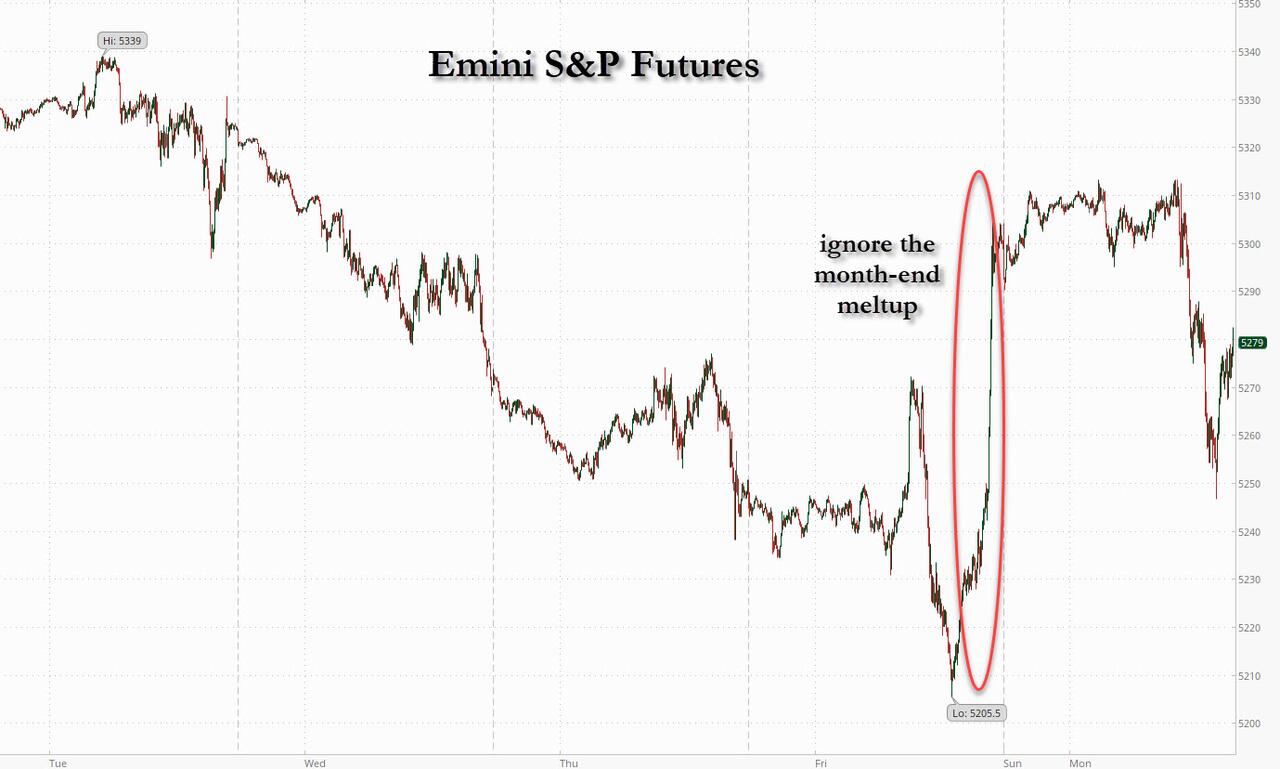

… and equities drifted lower for a 3rd straight day (excluding that glorious last-minute month-end rebel meetup last Friday)…

{kind=link}

… as something odd is going on: as The Market Ear flagged earlier, lately the Nasdaq has moved in the opposite direction of the US 10 year, which is unexpected since tech loves falling rates, prompting the traders to conclude that “something is changing”…

{kind=link}

More from The Market Ear.

Something is happening in cross-asset as we speak, and we do not like the smell of it

— The Market Ear (@themarketear) June 3, 2024

Maybe stagflation fears are becoming concerning for Wall Street…

ISM Manufacturing Survey Signals Further Stagflation: Growth Slows, Prices Rise https://t.co/jwshu6ekHN

— zerohedge (@zerohedge) June 3, 2024

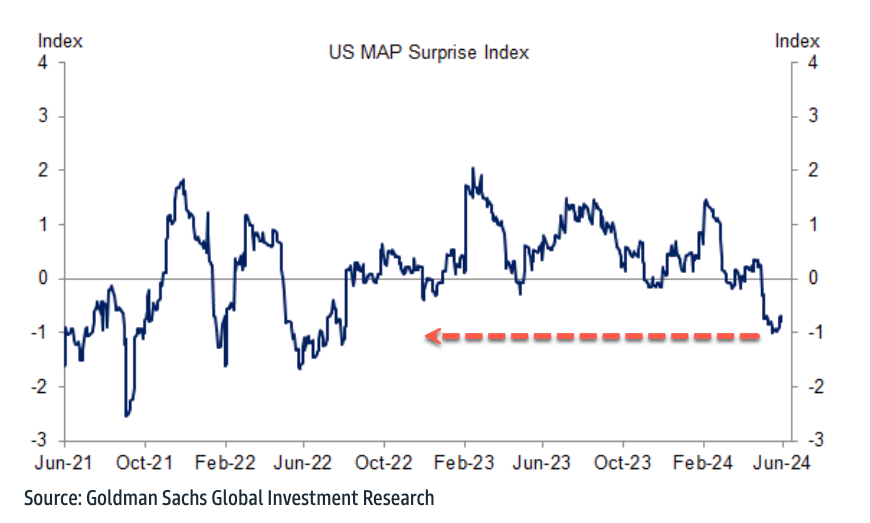

After all, the US economic surprise is back at summer 2022 lows.

{kind=link}

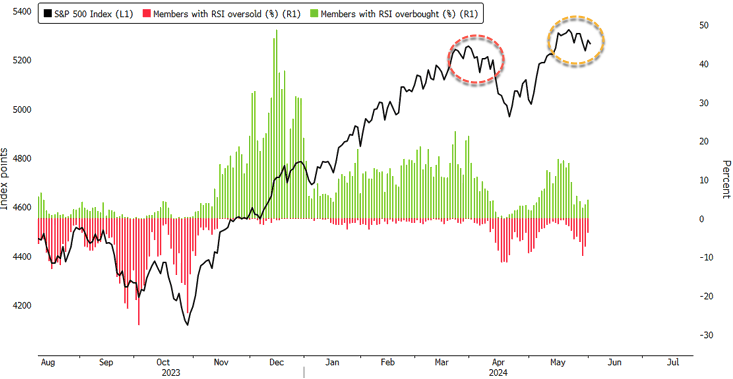

S&P500 has bad breadth.

{kind=link}

Is Dow Jones leading tech into another selloff?

{kind=link}

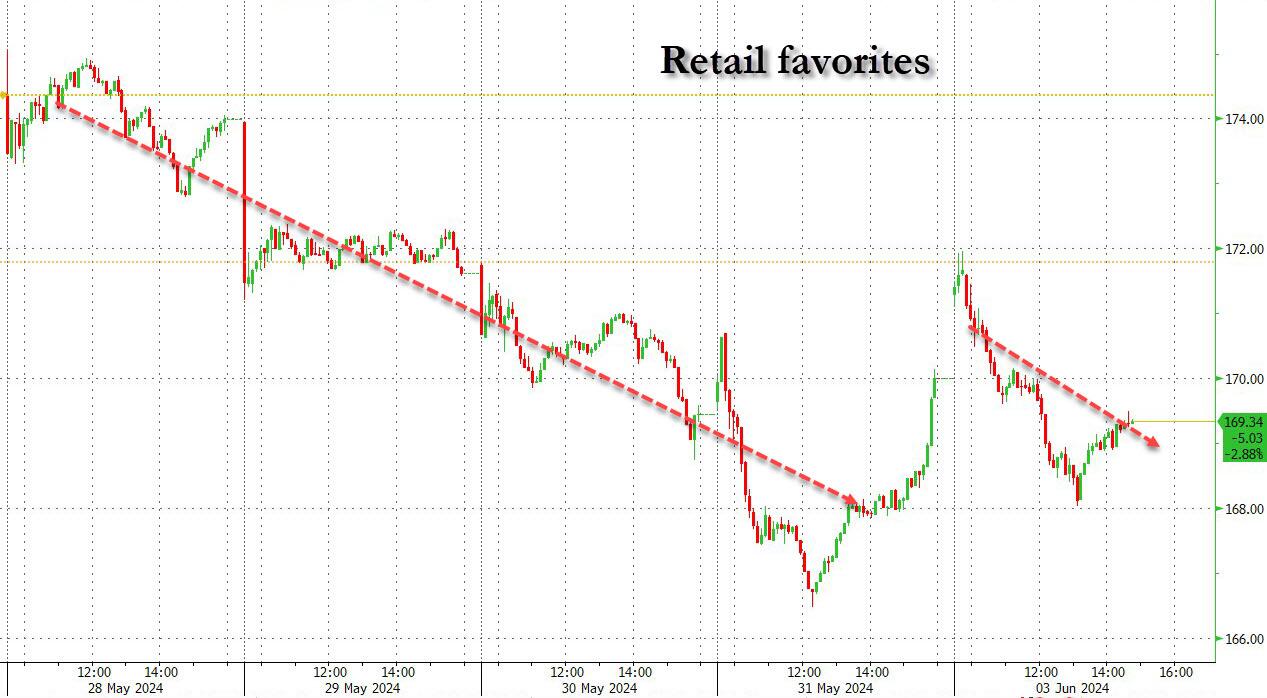

In any case, retail MoMo also weighed on sentiment as the opening meetup in the meme universe quickly reversed, and retail favorite stocks slumped…

{kind=link}

More broadly, Reddit traders should’ve just rolled their losses into Mag7 stocks after the meme bubble imploded in 2022.

{kind=link}

… Momentum continued to take on water, sliding -1% which now makes -3% in 3 sessions (although, as Goldman notes, this trade has failed to meaningfully unwind over the last 3 months and debates around AI sustainability coupled with Software weakness, alongside slower growth and lighter inflation data, all will be key elements for this factor), with the most shorted names continued the recent rebound after the late May rout.

{kind=link}

Finally, cyclical stocks were under big pressure following the dismal ISM print, and the GS cyclicals vs. defensives pair trade had their 2nd worst session of the year, as the basket slide to the lowest level since February.

{kind=link}

That said, activity was rather subdued, with market volumes down -9% vs the 10dma, even though Goldman’s trading desk reports that overall activity levels were up +24% vs. the trailing 2 weeks.

Some more details from the Goldman desk:

Floor tilts -1.5% better for sale, but HFs are net sellers and LOs are net to buy

HFs tilt -4.5% for sale, that ranks 75th %-ile over the last 1yr. Supply heaviest in Tech, HCare & Staples with modest demand for Comm Svcs, Fins, Mats & Disc.

LOs are +7.5% to buy and moving in the opposite direction of HFs – buying Tech, HCare & Staples vs selling Industrials, Utes, Mats & Energy.

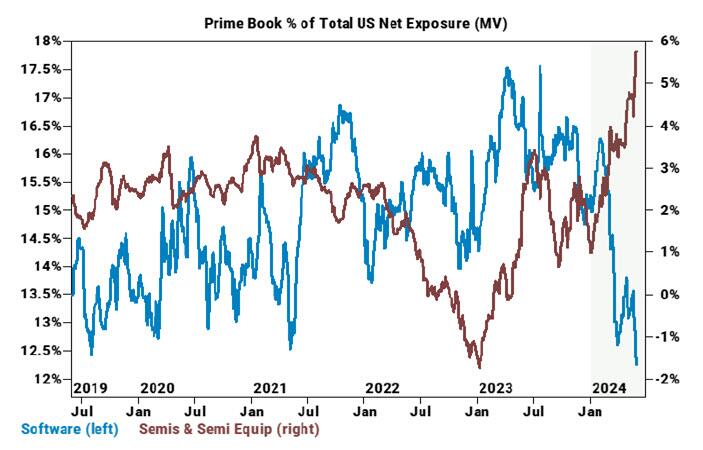

This reaffirms what we noted over the weekend when we pointed out that according to Goldman’s Prime Brokerage, hedge funds have turned very bearish lately and last week saw the biggest shorting of tech stocks in the past 11 weeks, led by software names.

{kind=link}

While stocks meandered, for crude, it was an unequivocal one-way street: the commodity crumbled as soon as traders walked in this morning, and then crashed after the disappointing ISM and Construction spending print, as oil remains the only asset that is pricing in a recession while every other asset classes is pricing in a soft landing.

{kind=link}

Meanwhile, the narrative surrounding the latest OPEC+ decision confirms that the market remains in sell-everything mode, as summarized below:

OPEC cuts output: “OPEC knows the economy is a disaster, trying to limit supply, oil prices will crash”

OPEC plans on gradually raising output: “OPEC cohesions is collapsing, OPEC no longer able to limit supply, prices will crash”

— zerohedge (@zerohedge) June 3, 2024

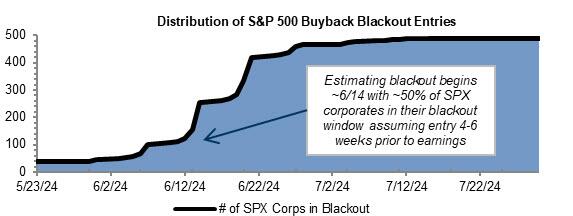

Yet despite the early rug pulls, it was a rather lackluster day, and with hedge funds and LOs pulling back, keeping the party going was all thanks to stock buyabcks. Speaking of, Goldman writes that it saw another active week on the buyback desk with volumes finishing 2.4x vs 2023 YTD ADTV and 1.3x vs 2022 YTD ADTV skewed toward Tech, Financials, and Consumer Discretionary. More importantly, the bank warns that while buybacks will dominate to the tune of about $5BN per day for the next two weeks, in mid-June we will enter the next blackout period, which if past is prologue, signals the next market swoon is imminent.

{kind=link}

But not yet: as the bank concludes, “In terms of our desk flows, we continue to see an increased number of discretionary buyback orders on the desk as the majority of companies remain in an open period.”

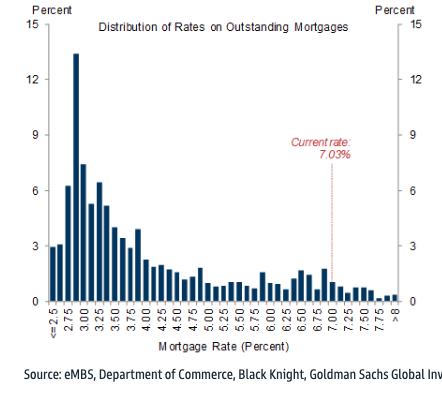

In another impressive chart (in the real estate world), Goldman’s Chris Hussey says, “95% of mortgage borrowers carry interest rates below current market rates, and almost 80% have rates 2pp below market rates, strongly disincentivizing them from moving since when they do, they will need to pay down the low-rate mortgage and take on a new, much higher-rate mortgage.”

{kind=link}

With the earnings season mostly over, traders will shift their attention to whether inflation is heating up again or continuing to decelerate.

Chris Larkin at E*Trade from Morgan Stanley said, “This week’s jobs report represents the next big test.”

The jobs report comes ahead of next week’s Federal Reserve meeting, with the swaps market showing no signs of interest rate cuts anytime soon. There are 1.65 cuts priced in by the end of the year, with the first possible in November.

{kind=link}

The Market Ear is correct. Something beneath the surface of the market is shifting.

Tyler Durden

Mon, 06/03/2024 – 16:00

Share This Article

Choose Your Platform: Facebook Twitter Linkedin