Time For A Reality Check?

Via Rabobank,

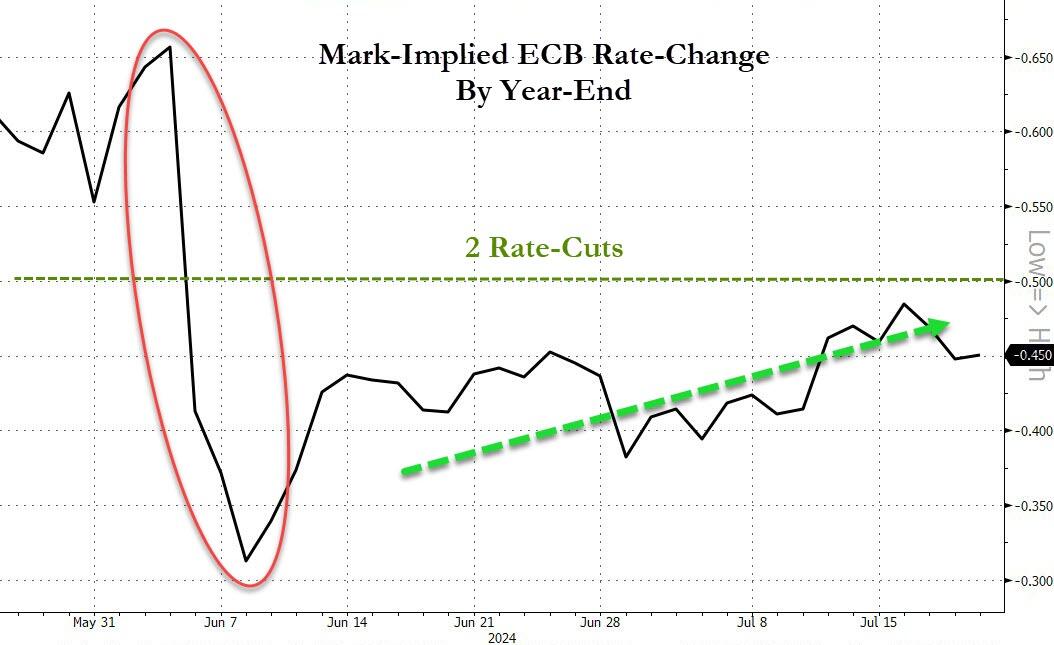

After a hawkish cut in June, the ECB dovishly held policy unchanged yesterday. To some extent that may be by design. Last month, the hawkish elements of the policy statement moderated market expectations of follow-up cuts. Yesterday’s dovish statement confirms that the ECB is still looking to cut rates, but in a measured pace.

Yet, Lagarde’s dovish remarks also appeared to reflect some genuine optimism regarding the inflation outlook. The elevated rate of wage growth did not surprise the Governing Council; the President pointed out that this has been factored into their latest projections. And the Governing Council concluded that companies’ profit margins are absorbing these higher labour costs. More importantly, she reiterated that “everything we see” currently indicates that wage growth will moderate in 2025 and 2026.

In the wake of the meeting, Bloomberg and Reuters reported different takes on the Governing Council’s deliberations. Bloomberg reported that policymakers are becoming less confident that they can cut twice more this year, although none of Bloomberg’s sources wanted to exclude the possibility of a rate cut in September. Reuters concluded that even some of the more hawkish policymakers are open to a September cut, provided that data confirm that disinflation is continuing.

{kind=link}

We conclude that the Governing Council is still inclined to look through near-term data, and that policymakers are willing to accept some setbacks as long as their longer-term outlook isn’t materially affected. This doesn’t mean that the ECB has abandoned its data-driven approach. Policymakers will reassess their outlook if the data prove them wrong, but the bar for that appears to be somewhat higher than before as more weight is attached to the ECB’s medium-term outlook.

Despite this growing importance of the medium-term outlook, Lagarde ironically refused to “speculate” on the implications of a potential Trump victory on the Eurozone growth and inflation outlook. She did acknowledge that that policymakers have to “take into account” the possibility of tariffs, but she did not specify how.

Recall that the ECB, like most official institutions, generally does not include assumptions of policy change into their forecasts until the policies have been announced.

Is it time for a reality check?

Because a Trump victory looks more likely after the attempt on his life last weekend.

Before he was escorted off the stage at a campaign rally, a wounded Trump stood and defiantly punched the air, producing what is sure to be the defining image of the campaign.

Meanwhile, the Democrats are in disarray.

President Biden is facing increasing pressure from high-ranking party members that want him to pull out of the race.

Speculation is rife that he may do so this weekend.

But even if he does, the question remains whether another candidate can quickly fill the leadership gap.

{kind=link}

Trump has been clear how he feels about tariffs:

“Economically, it’s great. And man, is it good for negotiation.”

His choice for running mate, JD Vance, is equally in favour of across-the-board tariffs in order to revive US-made goods.

Another term for Trump may also have big implications for the global security order.

It’s clear that Trump is not happy with other countries hiding behind the US military umbrella:

“I think, Taiwan should pay us for defense. You know, we’re no different than an insurance company.”

But Taiwan can rest assured: Europe has their back. Yesterday, Ursula von der Leyen was re-elected for president of the European Commission.

As part of her bid for the job, she said that she would “seek to deter China” from invading Taiwan.

But to quote Private Frost from Aliens:

“What we supposed to use, man, harsh language!?”

After all, the EU wasn’t able to deter Russia either.

And considering Trump’s stance towards Taiwan, the EU should probably be more concerned about their own defence first.

Von der Leyen at least seems to be aware of the urgent need to improve Europe’s military power:

“Combined EU spending on defence from 2019 to 2021 increased by 20%,” she said.

“In that time, Russia’s defence spending increased by almost 300% and China’s by almost 600%.”

Day ahead

Daily life is currently being disrupted by what appears to be an outage at a cybersecurity services provider. My Australian colleague is reporting that media, supermarkets, and banks are affected, including the payment cards. In Europe, airports, railways, and media companies have also reported disruptions. This may not be a hack or cyberattack; there have been earlier instances where a faulty update has taken down an entire cloud service provider, for example. Still, it highlights the vulnerabilities of today’s IT systems where key services are provided by just a handful of companies.

Other than that, it’s a quiet Friday in terms of data. Several ECB speakers have already sought out the press to provide their take on yesterday’s meeting and the outlook for monetary policy, and I suspect we’ll get more soundbites later today.

Tyler Durden

Fri, 07/19/2024 – 10:50

Share This Article

Choose Your Platform: Facebook Twitter Linkedin