“It Looks Like A VaR Shock To Me”: Gilts, Pound Crash Amid Panic Over Unsustainable UK Deficit

As we warned yesterday in our review of the just announced UK Budget (see “UK Gilt Yields Soar After Reeves Reveals Budget: Market Braces For Inflationary Debt Surge“), debt has always been the UK’s Achilles’ heel. That’s because “while the US has the world’s reserve currency, the UK doesn’t have that privilege, only an ability to print as much of a currency that fewer and fewer people want. That’s potentially very inflationary in the longer term, and that’s precisely why the market is reacting the way it is.”

Our bottom line was that with markets once again waking up to the likelihood that rates in the UK aren’t likely to fall as much previously expected, or the BOE would want, and should the blow out in yields continue, we may be just days away from another emergency QE action by the BOE in the past two years as the world is reminded that the only reason why the US can and continues to borrow like a drunken sailor, is because it still has the world’s reserve currency, although judging by the explosion in gold and bitcoin in recent days, that won’t last long.

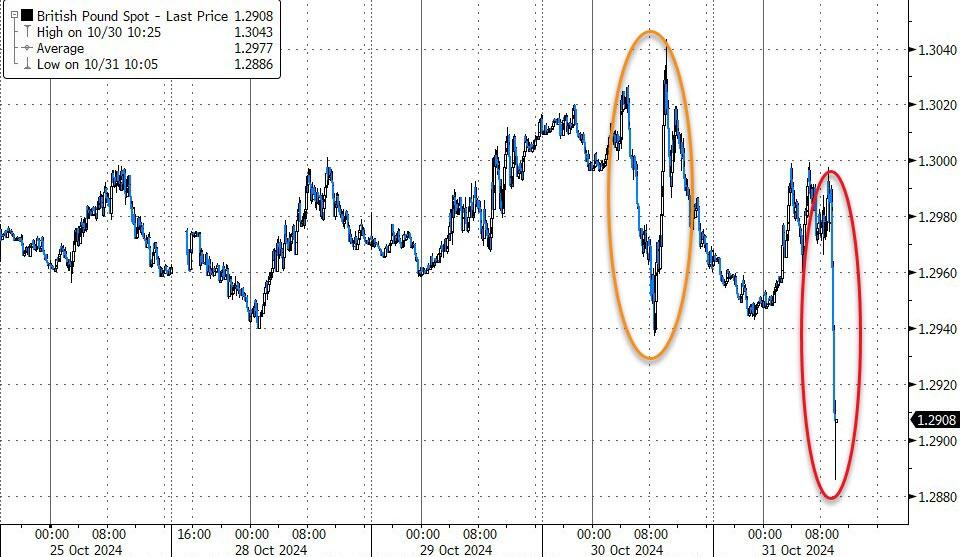

This morning we are getting confirmation that we may have been right once more, because both 2Y and 10Y Gilt yields are blowing out, and trading literally on top of each other as the entire gilt curve pancakes. The 10Y is trading at the highest level since Oct 2023, while the 2Y is back to May levels.

{kind=link}

The sudden blowout is not just confined to gilts however: as UBS trader Leo He notes, as the UK 2y yield is spiking, GBPUSD is selling off sharply.

{kind=link}

“It looks like a VaR shock to me”, He warns, and adds that “the US 2y yield is following the sharp rise in the UK 2 yield.”

No wonder why we used a lettuce for teaser image for our budget review post.

Commenting on the huger move in gilts, DB’s Jim Reid agrees with our take and writes this morning that “the main catalyst was that markets realized the true scale of the fiscal easing, as the UK Debt Management Office’s (DMO) revised gross financing needs were twice (c.£146bn) what DB expected between 2025-2029.”

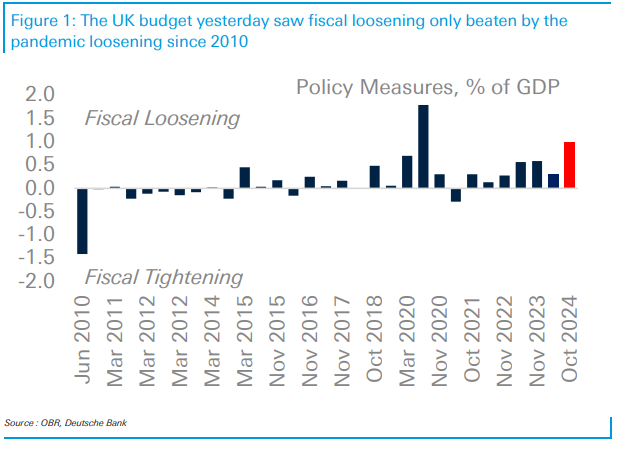

As DB’s economist Sanjay Raja noted in his review here, “today’s budget marks one of the largest fiscal loosening of any fiscal event in decades”.

Surprising it took the market one full day to figure it out.

Anyeay, the chart below from DB’s Sanjay shows that the only bigger fiscal loosening in the last decade-and-a-half was the pandemic easing.

{kind=link}

As Reid notes, it is interesting that 10yr Gilts are now only 10bps lower than the closing peak two business days after the ill-fated “mini-budget” under PM Liz Truss back in September 2022. On the day of that budget, they climbed around 42bps and then 26bps the following day. In terms of comparing the two budgets, in 2022 there were £45bn of unfunded tax giveaways, whereas yesterday’s had £32bn of unfunded commitments. One could argue the credibility of yesterday’s is enhanced by around 1/3rd of increased government spending being targeted for investment in the economy rather than the tax cuts of two years ago.

As Reid further reminds us, the Truss mini-budget would have been a complete reversal of economic policy in the UK, with a massive package of tax cuts, just as the Fed was still raising rates by 75bps while inflation remained high. They’d also just announced a significant energy price guarantee a couple of weeks earlier. So it was fuel to a fire, and then the LDI pension crisis occurred and the Bank of England intervened, with Truss standing down as PM shortly after.

The market reaction to yesterday’s budget probably wasn’t helped by strong European data pushing up yields on the continent and with general upward pressure on US yields as Trump looks to have generally improved his standing in the polls in recent weeks.

Still, let’s put this all in perspective: the UK budget deficit between 2025 and 2029 is expected to average around 2.5% of GDP. In the US, it could be 7-9% without offsetting measures to the campaign promises of the two candidates. This, Reid echoes our note from yesterday, “helps highlight the exorbitant privilege of the US in having the world’s reserve currency.”

After all, other countries with smaller deficits are starting to hit debt and deficit levels where markets are now raising their eyebrows (and term premia) as a minimum and concern (in the case of 2022) at the extremes. The continuing French budget issues are another example of this.

So in conclusion, yesterday’s budget was probably two-thirds of the Truss mini-budget, in terms of a fiscal easing but rather than biased towards tax cuts the bulk of the higher borrowing is due to a lot more investment, albeit ones that aren’t expected to bear fruit in growth terms until after the 5yr time horizon.

Tyler Durden

Thu, 10/31/2024 – 10:24

Share This Article

Choose Your Platform: Facebook Twitter Linkedin