Key Events This Extremely Busy Week: Jobs, JOLTS, PCE, GDP, And Peak Earnings

Welcome to what is without doubt the busiest two-week stretch of the year, starting with a barrage of earnings, payrolls, JOLTS, GDP, PCE and the Treasury refunding, and concluding with next week’s presidential election.

But first a look at the recent action, which as DB’s Peter Sidorov wraps up, saw the festive mood that dominated this fall suffer a mini-scare last week, as the S&P 500 fell for the first time in six weeks while the bond sell-off continued apace. And there’ll be plenty to test the market nerves with this week’s bumper set of data releases, including US payrolls on Friday, and earnings reports, with five of the Magnificent 7 reporting. Meanwhile, the tight US election campaign will enter its final stretch.

One market fear that has eased over the weekend is escalation risks in the Middle East. This comes as overnight into Saturday Israel carried out retaliatory strikes against Iran, but with these targeting military facilities and avoiding oil or nuclear installations. The targeted scope of the attack and the absence of an immediate retaliation signal have seen markets price out some of the geopolitical risk premium. Brent crude is down around -6% lower to below $72/bbl, reversing all of last week’s rise; Gold is down -0.60% from Friday’s record high, while US equity futures are posting decent gains.

Meanwhile, Treasuries extended their recent decline, with 10yr yields at one point rising as high as 5bps to 4.29% as I type, their highest level since July, having now risen by 65bps from their September lows, although the move is now reversing. This rise has come amid both rising term premia, partly driven by concerns about US fiscal deficits, and growing skepticism that the Fed will deliver rapid rate cuts given solid US data. Indeed, Fed funds futures for end-25 are up to 3.53% this morning, having priced out three 25bps cuts over the past six weeks.

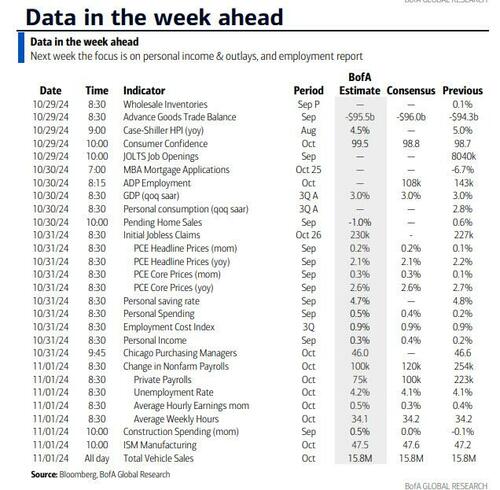

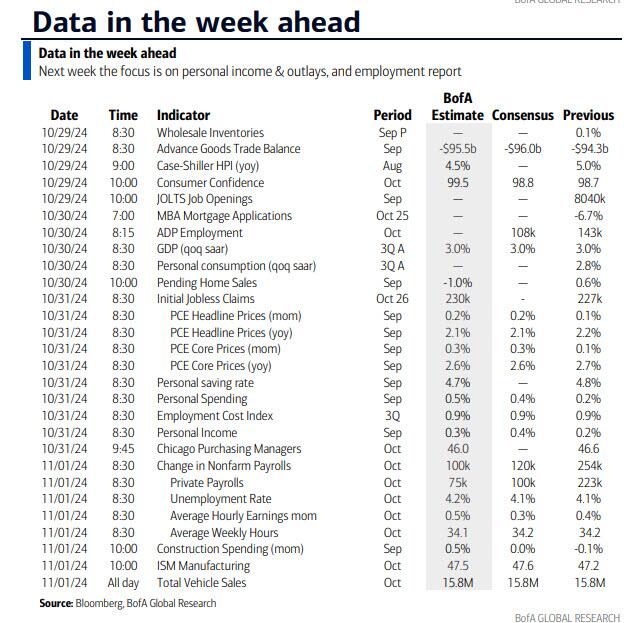

With the Fed now in the blackout period ahead of next Thursday’s meeting, the data will be doing the talking this week, with the marquee release being the October payrolls report on Friday. Most economists foresee a sizeable slowing in headline (consensus expects +110k jobs vs. 254k previously) and private (+90k vs. 223k) payrolls. However, this envisages a nearly -70k drag due to striking workers (mostly Boeing) and the weather impact of Hurricane Milton. The weather effect will have less of an impact on average hourly earnings (+0.3% vs. +0.4%), while unemployment is expected to remain unchanged at 4.1% amid unchanged labor force participation. Given the likely noise in the payrolls, the market may pay extra attention to Tuesday’s JOLTS report for September. Given the strong September payrolls, the hiring rate may pick up from the historically low 3.3% in August. The last JOLTS print also saw the quits rate, one of the best leading indicators of wage growth, fall to 2.1%, its weakest since 2015 if one excludes the first few months of Covid. Other labor market data will include the Q3 Employment Cost Index reading (DBe: +0.9% vs. +0.9%), which is the Fed’s preferred measure of wage growth.

In other US data, traders will pay attention to the September personal income release on Thursday, which includes the Fed’s preferred core PCE inflation measure. Consensus expects core PCE inflation to rise by +0.3% (vs. +0.13% previously), its strongest since March. And Wednesday’s advance Q3 real GDP is expected to show continued solid growth (+3.0% vs. +3.0% in Q2). On the fiscal side, we have the US Treasury refunding announcement, with borrowing estimates on Monday and the refunding policy statement on Wednesday.

{kind=link}

Over in the euro area, the highlights will be the Q3 GDP print on Wednesday and the October flash inflation release on Thursday, with the latter preceded by the Spain and Germany CPI prints on Wednesday. Our European economists see headline euro area inflation rising from 1.7% to 1.9% but with core inflation slowing by a tenth to +2.6%, which would be its lowest level since January 2022. See our economists Inflation Chartbook here for more.

In the UK, the focus will be on the Autumn Budget on Wednesday. This will be the Labor Government’s first budget in almost 15 years and as reviewed last week, it will literally change the definition of debt so the UK can raise more of it. Over in Asia, we will have the latest BOJ decision on Thursday, where a hold is widely expected despite the plunge in the yen today. And in China, the official PMIs on Thursday and the Caixin manufacturing PMI on Friday will be closely watched to gauge the effectiveness of the stimulus measures outlined by Beijing over the past month.

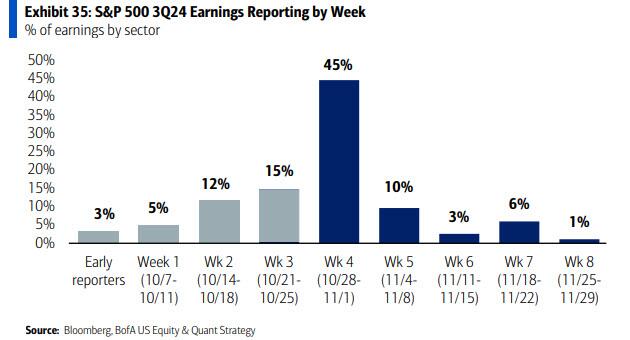

It will be a bumper week for earnings, with more than 40% of the S&P 500 by market cap expected to report.

{kind=link}

Following on the blockbuster earnings report from Tesla last week, five more of the Magnificent 7 are reporting this week, including Alphabet (Tuesday), Microsoft and Meta (Wednesday), Apple and Amazon (Thursday). See the rest of the week’s earnings and data releases in the day-by-day calendar at the end.

{kind=link}

Last but certainly not least, the US election campaign will enter its final week ahead of the next Tuesday’s vote. Over 40 million early votes have already been cast and the latest polls continue to show a very tight race. The FiveThirtyEight average gives Harris a 1.5pp lead in national polls, but with a 0.6pp lead for former President Trump on average across the seven swing states, all of which see leads of less than 2pp for either candidate. The RealClearPolitics betting average now has former President Trump with a 61% likelihood of victory. That’s the highest it’s been since President Biden dropped out of the race in July, though it has largely stabilized in the past week.

Courtesy of DB, here is a day-by-day calendar of events

Monday October 28

Data: US October Dallas Fed manufacturing activity, UK October Lloyds Business Barometer, Japan September jobless rate, job-to-applicant ratio

Central banks: ECB’s Wunsch speaks

Earnings: Waste Management, Cadence Design Systems, Ford

Auctions: US Treasury quarterly borrowing estimates, 2-yr Notes ($69bn), 5-yr Notes ($70bn)

Tuesday October 29

Data: US September JOLTS report, advance goods trade balance, wholesale inventories, October Conference Board consumer confidence index, Dallas Fed services activity, August FHFA house price index, UK September net consumer credit, M4, Germany November GfK consumer confidence, Sweden September GDP indicator

Earnings: Alphabet, Visa, Novartis, AMD, McDonald’s, Pfizer, Stryker, Chubb, American Tower, Mondelez, BP, PayPal, Chipotle Mexican Grill, adidas, Reddit, Covestro, Davide Campari-Milano

Auctions: US 2-yr FRN ($30bn), 7-yr Notes ($44bn)

Wednesday October 30

Data: US October ADP report, Q3 GDP, September pending home sales, Japan October consumer confidence index, September retail sales, industrial production, Germany October CPI, unemployment claims rate, Q3 GDP, France Q3 GDP, September consumer spending, Italy Q3 GDP, September PPI, Eurozone October services, industrial and economic confidence, Q3 GDP, Australia Q3 CPI

Central banks: ECB’s Schnabel and Nagel speak

Earnings: Microsoft, Meta, Eli Lilly, AbbVie, Caterpillar, Amgen, Booking, Airbus, Hitachi, BYD, Starbucks, GSK, Volkswagen, BASF, Humana, eBay

Other: UK budget

Auctions: US Treasury quarterly refunding announcement

Thursday October 31

Data: US September PCE, personal income and spending, Q3 employment cost index, October MNI Chicago PMI, initial jobless claims, China October official PMIs, Japan September housing starts, Germany September retail sales, import price index, France October CPI, September PPI, Italy October CPI, September unemployment rate, August industrial sales, Eurozone October CPI, September unemployment rate, Canada August GDP

Central banks: BoJ decision, ECB’s economic bulletin, Panetta speaks, BoE’s Breeden speaks

Earnings: Apple, Amazon.com, Mastercard, Merck & Co, Samsung Electronics, Linde, Shell, Uber, Comcast, TotalEnergies, Eaton, AB InBev, ConocoPhillips, Regeneron Pharmaceuticals, Bristol-Myers Squibb, Intel, Cigna, Altria, Cheniere Energy, Blue Owl Capital, Estee Lauder, Kellanova, Roblox, STMicroelectronics, AP Moller – Maersk

Friday November 1

Data: US October jobs report, ISM index, total vehicle sales, September construction spending, China October manufacturing Caixin PMIs, Canada October manufacturing PMI, Switzerland October CPI

Earnings: Exxon Mobil, Chevron, Charter Communications, Ares

* * *

Looking at just the US, Goldman writes that the key economic data releases this week are the Q3 GDP advance release on Wednesday, the core PCE inflation and the employment cost index on Thursday, and the employment report on Friday. There are no policy-related speaking engagements from Fed officials this week, reflecting the blackout period ahead of the November FOMC meeting.

Monday, October 28

There are no major economic data releases scheduled.

Tuesday, October 29

08:30 AM Wholesale inventories, September preliminary (consensus flat, last +0.1%)

08:30 AM Advance goods trade balance, September (GS -$97.5bn, consensus -$95.9bn, last -$94.3bn)

09:00 AM FHFA house price index, August (consensus +0.2%, last +0.1%)

09:00 AM S&P Case-Shiller 20-city home price index, August (GS +0.2%, consensus +0.2%, last +0.3%)

10:00 AM JOLTS job openings, September (GS 7,900k, consensus 7,935k, last 8,040k): We estimate that JOLTS job openings edged slightly lower in September (-0.1mn to 7.9mn), reflecting moderation in online job postings.

10:00 AM Conference Board consumer confidence, October (GS 98.8, consensus 99.0, last 98.7)

Wednesday, October 30

08:15 AM ADP employment change, October (GS +115k, consensus +110k, last +143k); We forecast a 115k increase in ADP employment in October, 20k above our October nonfarm payroll forecast of 95k. While ADP does not benefit from continued catch-up hiring in the government sector as it only covers private employment, it has historically been less sensitive to striking workers (we assume a 41k drag on nonfarm payrolls from newly striking workers) and natural disasters (we assume a 40-50k drag on nonfarm payrolls from the recent hurricanes).

08:30 AM GDP, Q3 advance (GS +3.0%, consensus +3.0%, last +3.0%); Personal consumption, Q3 advance (GS +3.5%, consensus +3.2%, last +2.8%); Core PCE inflation, Q3 advance (GS +2.03%, consensus +2.1%, last +2.8%): We estimate that GDP rose 3.0% annualized in the advance reading for Q3, following +3.0% annualized in Q2. Our forecast reflects strength in consumption (+3.5%, quarter-over-quarter annualized) and business fixed investment (+6.4%), supported by a 13.3% increase in equipment investment, as well as a rebound in exports (+8.0%) that more than offset a slowdown in residential investment (-4.6%) and another quarter of strong imports growth (+7.6%). We estimate that the core PCE price index increased 2.03% annualized (or 2.65% year-over-year) in Q3.

10:00 AM Pending home sales, September (GS +1.8%, consensus +1.3%, last +0.6%)

Thursday, October 31

08:30 AM Personal income, September (GS +0.4%, consensus +0.3%, last +0.2%); Personal spending, September (GS +0.4%, consensus +0.4%, last +0.2%); Core PCE price index, September (GS +0.25%, consensus +0.3%, last +0.1%); Core PCE price index (YoY), September (GS +2.61%, consensus +2.6%, last +2.7%); PCE price index, September (GS +0.16%, consensus +0.2%, last +0.1%); PCE price index (YoY), September (GS +2.05%, consensus +2.1%, last +2.2%): We estimate personal income and personal spending both increased by 0.4% in September. We estimate that the core PCE price index rose by 0.25%, corresponding to a year-over-year rate of 2.61%. Additionally, we expect that the headline PCE price index increased by 0.16% from the prior month, corresponding to a year-over-year rate of 2.05%. Our forecast is consistent with a 0.16% increase in our trimmed core PCE measure (vs. +0.14% in August).

08:30 AM Employment cost index, Q3 (GS +0.9%, consensus +0.9%, last +0.9%): We estimate the employment cost index rose by 0.9% in Q3 (quarter-over-quarter, seasonally adjusted), which would lower the year-on-year rate by one tenth to 4.0% (year-over-year, not seasonally adjusted). Our forecast reflects deceleration in the average hourly earnings of production and nonsupervisory workers and the Atlanta Fed’s wage tracker. We also expect a slower pace of ECI growth among unionized workers—following 1.6-1.7% increases on average in Q4-Q2 (SA by GS, not annualized)—and a moderation in ECI benefit growth after resetting higher in the first half of the year (0.9% vs. 1.1% in Q1 and 1.0% in Q2). On the positive side, we expect slightly firmer compensation for incentive-paid occupations after it underperformed broader compensation growth in Q2.

08:30 AM Initial jobless claims, week ended October 26 (GS 225k, consensus 232k, last 227k); Continuing jobless claims, week ended October 19 (consensus 1,878k, last 1,897k)

09:45 AM Chicago PMI, October (GS 48.0, consensus 47.0, last 46.6)

Friday, November 1

08:30 AM Nonfarm payroll employment, October (GS +95k, consensus +110k, last +254k); Private payroll employment, October (GS +70k, consensus +90k, last +223k); Average hourly earnings (MoM), October (GS +0.3%, consensus +0.3%, last +0.4%); Average hourly earnings (YoY), October (GS +4.0%, consensus +4.0%, last +4.0%); Unemployment rate, October (GS 4.1%, consensus 4.1%, last 4.1%); Labor force participation rate, October (GS 62.7%, consensus 62.7%, last 62.7%): We estimate nonfarm payrolls rose 95k in October. Big Data indicators indicated a sequentially softer pace of job creation, and we estimate the recent hurricanes weighed on October job growth by 40-50k. The Bureau of Labor Statistics indicated that newly striking workers, including those at Boeing, will exert a 41k drag on October payroll growth. We assume above-trend (albeit moderating) contributions from the recent surge in immigration and catch-up hiring. We estimate that the unemployment rate was unchanged at 4.1%, reflecting a flat labor force participation rate and solid household employment growth. We estimate average hourly earnings rose 0.3% (month-over-month, seasonally adjusted), which would leave the year-over-year rate unchanged at 4.0%, reflecting a boost from the impact of the hurricanes but payback for unusually strong supervisory earnings in recent months.

09:45 AM Dallas Fed President Logan (non-FOMC voter) speaks; Dallas Fed President Lorie Logan will give welcoming remarks at the Women in Central Banking workshop, sponsored by the Dallas Fed. Speech text is expected.

09:45 AM S&P US Manufacturing PMI, October final (consensus 47.8, last 47.8)

10:00 AM ISM manufacturing index, October (GS 48.0, consensus 47.6, last 47.2): We estimate the ISM manufacturing index increased in October (+0.8pt to 48.0), reflecting sequential improvement in other manufacturing surveys (GS manufacturing survey tracker +1.3pt to 49.0) but a slight headwind from seasonality.

10:00 AM Construction spending, September (GS +0.2%, consensus flat, last -0.1%)

05:00 PM Lightweight motor vehicle sales, October (GS 16.0mn, consensus 15.8mn, last 15.8mn)

Source: DB. Goldman

Tyler Durden

Mon, 10/28/2024 – 09:53

Share This Article

Choose Your Platform: Facebook Twitter Linkedin